AI Agents for Insurance: Building the Next Generation of Digital Insurers

Table of contents

- Key takeaways:

- AI Agents for Insurance and Their Benefits

- What are AI agents for insurance?

- The strategic benefits of AI agents for modern insurers

- Autonomous task execution

- Higher agent productivity through human-AI collaboration

- Faster and more intelligent claims handling

- Continuous data analysis and real-time operational insights

- Always-on customer interaction

- Smarter lead qualification and sales support

- Proactive decision support for underwriting and risk assessment

- Agentic AI vs. Traditional Workflow Automation in Insurance

- The Building Blocks of an AI Agent in Insurance

- Goal: Defining the operational objective

- Context: Understanding operational and regulatory conditions

- Reasoning: Evaluating conditions and determining actions

- Tools: Enterprise systems the agent can use

- Controls: Governance, safeguards, and human oversight

- Top AI Agent Use Cases in Insurance

- AI claims processing agents

- Intelligent quote and sales automation agents

- 24/7 agentic customer support

- Hyper-personalized communication agents

- AI fraud detection and investigation agents

- Trust Architecture: How to Control Insurance AI Agents

- Deployment strategy: security and data sovereignty

- Audit trails and traceability (explainable AI)

- Tiered autonomy and human-in-the-loop governance

- What Can Go Wrong? Key Risks of Insurance AI Agents

- Regulatory and compliance risk

- Decision errors and hallucinations

- Bias and fairness concerns

- Data security and systemic dependency risk

- The Future of AI Agents in Insurance: Key Trends

- End-to-end autonomous insurance operations

- Real-time, dynamic, and event-driven insurance

- Continuous underwriting and adaptive pricing

- Multi-agent insurance ecosystems

- Conclusion

The insurance industry faces a critical inflection point: adapting to AI-driven change is now essential for survival. With autonomous AI, predictive analytics, and real-time intelligence transforming every aspect of operations and traditional models becoming more unsustainable, insurers who fail to evolve will struggle to:

- Meet customer expectations.

- Compete effectively.

- Deliver fast, personalized services.

Across the industry, insurers are shifting from reactive operations to more proactive and predictive models. These systems help organizations detect risks earlier, identify behavioral patterns, anticipate customer needs, uncover anomalies, and reduce operational losses before they escalate.

At the same time, customer acquisition is evolving rapidly. Consumers now rely on AI assistants to compare policies, assess coverage, and recommend products. As a result, insurance discoverability is no longer defined by advertising or search rankings; instead, it depends on how AI evaluates relevance, trustworthiness, pricing, and fit in real time.

Customer service is being redefined. Advanced conversational and voice technologies enable insurers to deliver personalized, context-aware support across digital channels. These interactions go beyond basic chatbots, allowing natural, human-like conversations that address complex requests.

Internally, insurers adopt agentic models where AI agents act as digital workers across underwriting, claims, fraud detection, compliance, document management, and communication. These systems now coordinate decisions, interact with platforms, manage exceptions, and adapt to change.

This transformation is measurable. McKinsey reports that AI-leading insurers generate shareholder returns 6.1 times higher than laggards, demonstrating how AI maturity drives performance.

Strategic discussions now extend beyond automation. Insurers ask: Which responsibilities can be delegated to intelligent systems and still ensure governance, compliance, explainability, and trust?

This article analyzes the business value of AI-driven insurance transformation, the differences between agentic AI and automation, and considerations for scaling AI while maintaining standards.

Key takeaways:

- AI agents enable insurers to automate complex workflows across claims, underwriting, fraud detection, customer service, and policy administration.

- Key business value includes faster claims, better customer service, enhanced fraud prevention, more accurate risk assessment, and lower costs.

- Effective adoption requires governance, explainability, human oversight, auditability, and compliance with industry regulations.

- Insurance is shifting toward interconnected agents, continuous underwriting, real-time risk management, and greater autonomy.

- Firms merging AI innovation with trust architectures will improve efficiency, competitiveness, and scalability in digital insurance.

AI Agents for Insurance and Their Benefits

Modern insurance operations require seamless coordination across various teams and technology systems, yet growing data volumes and fragmentation create new challenges. Traditional automation falls short of managing this complexity at scale. AI-driven orchestration stands out as the new solution, giving insurers powerful tools to improve efficiency, reduce complexity, and enable better decisions.

What are AI agents for insurance?

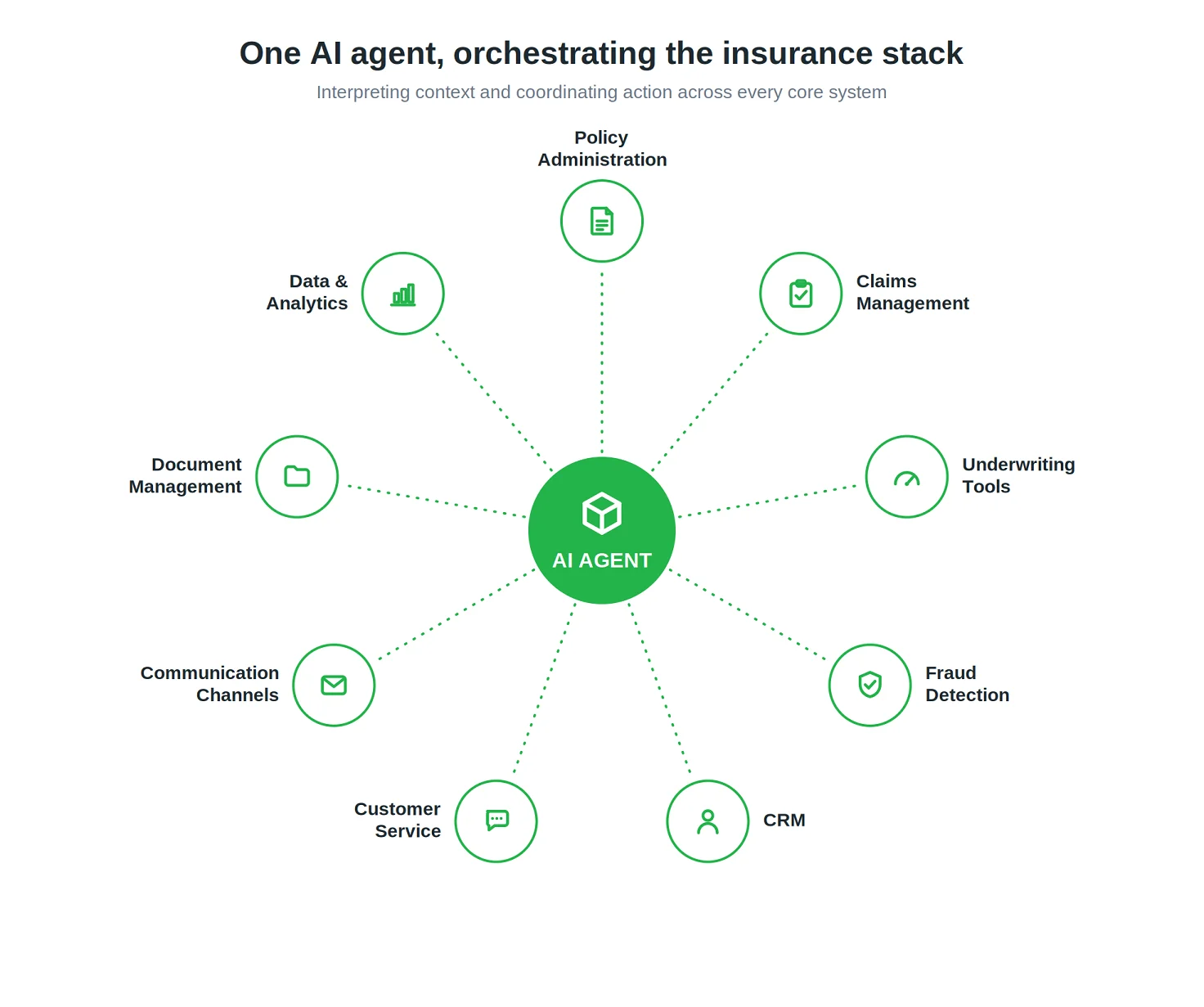

AI agents are intelligent software that autonomously or semi-autonomously analyze data, coordinate workflows, make decisions, and execute tasks in insurance. Unlike traditional automation, which uses rigid rules, AI agents interpret context, adapt to change, and interact with interconnected systems. These agents are guided by business rules, risk parameters, goals, and real-time data. In insurance organizations, AI agents may interact with:

- Policy administration systems

- Claims-management platforms

- CRM environments

- Fraud-detection systems

- Underwriting tools

- Customer-service platforms

- Communication channels

- Document-management systems

- Data and analytics environments

These systems process claims, retrieve policy details, evaluate risks, manage customer interactions, detect suspicious activity, generate documents, and automatically route exceptions.

Advanced environments use specialized agents across underwriting, claims, fraud prevention, compliance, customer engagement, and sales.

The shift toward AI-driven multi-agent orchestration delivers measurable improvements for insurers, namely, increased efficiency, responsiveness, scalability, and high-quality decision-making. As multi-agent AI becomes integral, its strategic value is clear.

The strategic benefits of AI agents for modern insurers

Strategically implemented AI agents empower insurers to operate more efficiently, automate tasks, improve decision quality, and deliver superior customer experiences. This positions insurers better in a competitive, data-driven environment.

Autonomous task execution

Routine insurance operations now require minimal human effort. Agents automatically handle claims intake, document checks, record updates, follow-ups, and policy workflows, which speed processing and reduces friction.

Higher agent productivity through human-AI collaboration

Rather than replacing insurance professionals, AI agents function as operational copilots that support employees in real time. By summarizing cases, retrieving policy details, drafting responses, and surfacing recommendations, these systems reduce repetitive administrative work and allow teams to focus on negotiation, customer relationships, and complex decision-making.

Faster and more intelligent claims handling

Claims operations involve fragmented documentation, repeated verifications, and lengthy coordination. AI-powered workflows gather documents, verify information, spot inconsistencies, pre-assess claims, and quickly route cases to the right teams.

Continuous data analysis and real-time operational insights

Modern insurance generates vast operational and behavioral data. AI agents monitor activity to spot anomalies, risks, suspicious patterns, and bottlenecks early.

Individualized customer experiences are easier with intelligent orchestration. By analyzing behaviors, policy history, preferences, and context, AI agents tailor recommendations, onboarding, reminders, and communications throughout the customer lifecycle.

Always-on customer interaction

24/7 digital support is now standard in insurance. AI assistants manage routine inquiries via chat, email, messaging, and voice. They are able to resolve most requests instantly and escalate complex cases to humans as needed.

Smarter lead qualification and sales support

Sales and distribution teams use intelligent lead prioritization and automated prospect analysis. By assessing behavior, engagement, and conversion likelihood, AI agents focus sales on top opportunities and improve utilization of resources.

Proactive decision support for underwriting and risk assessment

Underwriters use AI insights to speed and strengthen risk evaluation. Intelligent agents analyze customer profiles, behaviors, claim history, and risk factors to suggest pricing, find exposures, and support consistent decisions.

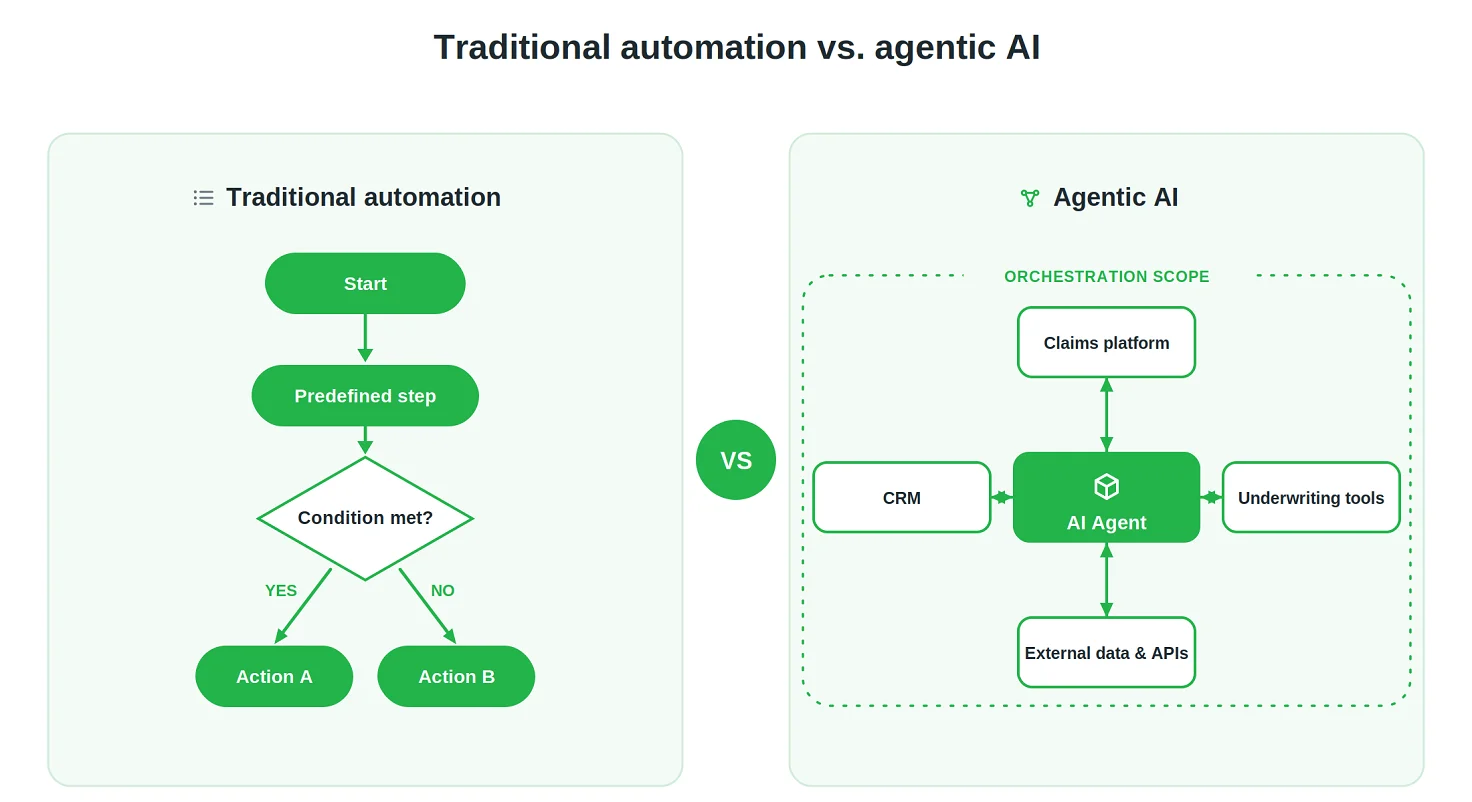

Agentic AI vs. Traditional Workflow Automation in Insurance

Insurance companies have traditionally adopted rule-based automation such as robotic process automation and chatbots to streamline repetitive tasks. These solutions deliver clear value for predictable, rules-based processes like policy administration, claims routing, and customer communications.

Yet, as the insurance environment evolves, traditional automation reveals limits. Insurers now must handle an increasing range of data types and volumes, shifting regulations, and higher expectations for personalized digital experiences. This exposes the gap where rigid automation cannot keep up with ambiguity or contextual needs.

AI agents address these challenges by providing adaptive operational intelligence. Rather than rigidly following rules, they interpret contexts, synthesize information, reason across scenarios, and execute coordinated actions. This enables end-to-end process management, informed decision-making, and smart escalation to humans when judgment is needed.

Crucially, agentic AI complements rather than replaces existing automation. By moving from task completion to orchestrating results across people, processes, and technology, AI agents help insurers realize broader business goals and maximize automation investments.

The following table summarizes the fundamental distinctions between traditional automation and agentic AI in the insurance industry.

| Feature | Traditional AI (chatbots and workflow automation) | AI agent (agentic AI) |

| Primary objective | Supports users by providing information, answering questions, or executing predefined workflow steps. | Works toward a business goal by coordinating activities, making decisions, and driving processes to completion. |

| Operating model | Reactive. Responds to user requests, predefined triggers, or workflow events. | Proactive and outcome-oriented. Identifies next steps and initiates actions required to achieve a target result. |

| Decision-making | Follows predefined rules, decision trees, and workflow logic. | Applies contextual reasoning, evaluates available information, and adapts decisions based on changing circumstances and business constraints. |

| System connectivity | Typically operates within a specific application or limited set of integrated systems. | Orchestrates activities across policy administration systems, claims platforms, underwriting tools, CRM solutions, external databases, and APIs. |

| Use of data | Relies primarily on information explicitly provided by users or available within predefined datasets. | Continuously collects, validates, and enriches data from multiple internal and external sources to support decision-making. |

| Claims processing example | A chatbot can provide status updates, such as: “Your claim has been received and is currently under review.” The system informs the customer but does not actively process the claim. | Reviews claim documentation, verifies policy coverage, requests missing information when necessary, gathers supporting evidence, and automatically initiates the next stages of the claims workflow. |

| Underwriting examples | Generates risk scores based on predefined criteria and application data. | Combines information from multiple sources, identifies potential risk indicators, gathers additional context, and provides evidence-based recommendations to support underwriting decisions. |

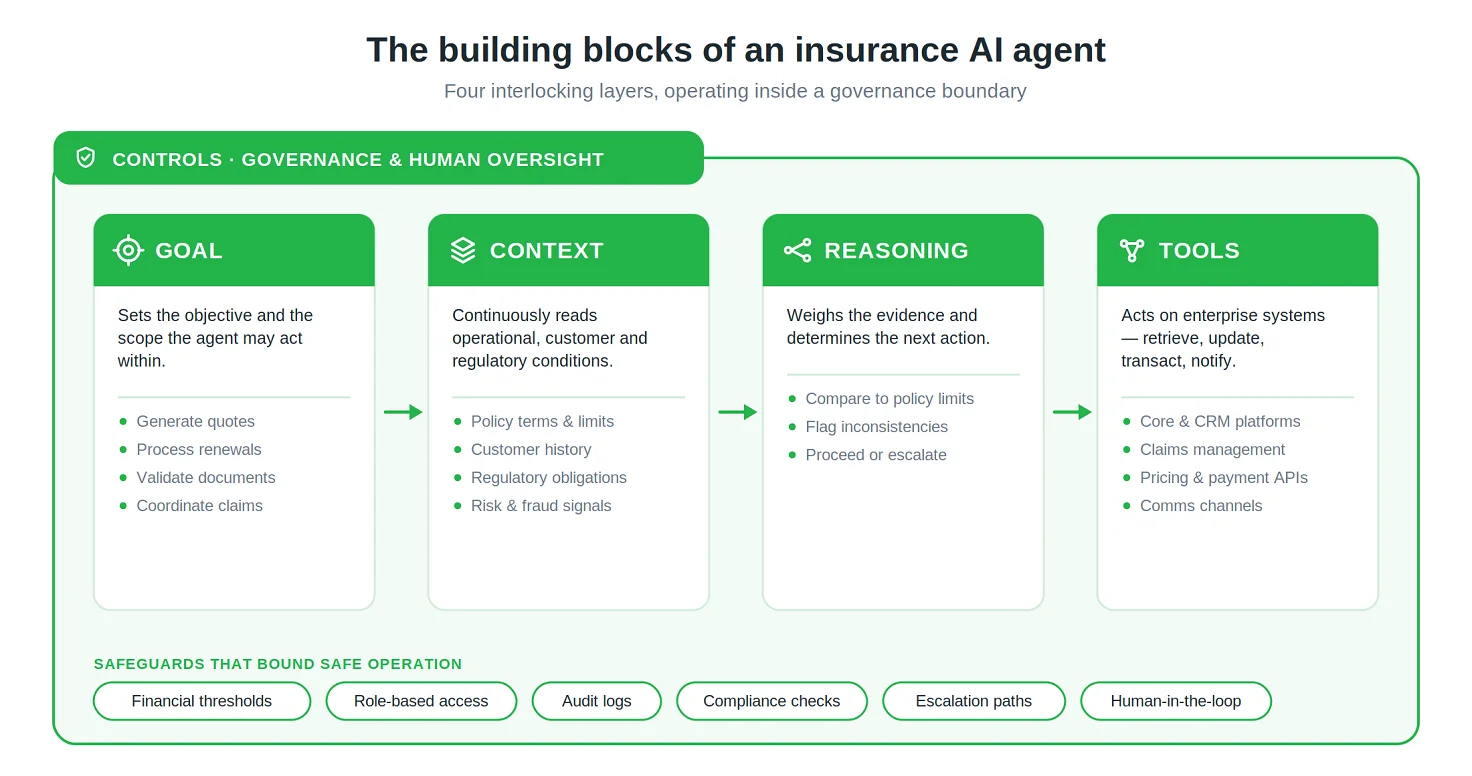

The Building Blocks of an AI Agent in Insurance

Insurance AI agents surpass chatbots and rule-based scripts by functioning as unified operational systems. By integrating reasoning, workflow orchestration, enterprise connectivity, contextual awareness, and strong governance, these agents directly support and automate the complex, regulated processes at the heart of insurance.

To reliably navigate highly regulated insurance environments, AI agents depend on foundational components that tightly interlock to serve a common goal. Each layer is critical for enabling the agent to understand business objectives, interpret context, make compliant decisions, interface with enterprise systems, and operate securely.

Goal: Defining the operational objective

Every AI agent in insurance is designed around a specific business objective. The goal establishes both the expected outcome and the operational scope within which the agent can act.

Depending on the use case, an agent may generate personalized insurance quotes, process policy renewals, validate submitted documentation, coordinate claims workflows, detect fraud indicators, or support claim-settlement procedures.

Clearly defined objectives are crucial, because insurance decisions often affect finances, compliance, and customer satisfaction. With well-structured goals, AI agents maintain predictability, measurability, and consistent alignment with business priorities.

Context: Understanding operational and regulatory conditions

Insurance workflows depend on contextual understanding instead of isolated data. Reliable AI agents continuously evaluate information across various operational, customer, and regulatory settings.

This contextual layer may include:

- Policy terms and coverage limitations

- Customer history and behavioral patterns

- Internal claims and underwriting procedures

- Regulatory obligations and compliance policies

- Pricing models and rate structures

- Risk indicators and fraud signals

For example, similar claims may need different handling based on policy exclusions, customer history, region, claim frequency, or coverage thresholds.

Without strong contextual awareness, AI agents cannot reliably achieve accurate or compliant decisions, undermining their value in real-world insurance operations.

Reasoning: Evaluating conditions and determining actions

Reasoning sets AI agents apart from traditional automation.

Rather than following static instructions, intelligent agents analyze data, assess business conditions, spot inconsistencies, and determine next steps based on logic and risk.

In insurance environments, this may involve:

- Evaluating reported damages or losses

- Comparing requests against policy limits and exclusions

- Detecting unusual behavioral or fraud patterns

- Identifying missing or inconsistent documentation

- Determining whether a case can proceed automatically or requires escalation

This adaptive reasoning layer equips insurers to manage operational complexity and ensures agents deliver consistent, business-aligned decisions across underwriting, claims, and service workflows.

Tools: Enterprise systems the agent can use

The real operational value of AI agents comes from their ability to interact directly with enterprise systems rather than simply generate recommendations.

Insurance AI agents may integrate with:

- Core insurance and CRM platforms

- Claims-management systems

- Risk-assessment and pricing tools

- Asset and collateral registries

- Payment gateway APIs

- Customer communication platforms

- Email, chat, and messaging environments

Integrations let agents retrieve data, update records, start processes, process transactions, coordinate communication, and sync operations across platforms.

The breadth and quality of integrations are primary factors determining how effectively the AI agent transforms insurance operations.

Controls: Governance, safeguards, and human oversight

Since AI agents affect claims, finances, compliance, and customer interactions, strong governance is essential.

Controls define the operational boundaries within which the agent can safely function.

These safeguards often include:

- Financial thresholds for automated decisions

- Access permissions and role-based restrictions

- Traceable audit logs and decision histories

- Compliance-validation mechanisms

- Fraud-detection controls

- Escalation workflows and exception management

- Human approval checkpoints (human-in-the-loop)

For instance, low-risk claims may be processed automatically, while high-value, suspicious, or legally sensitive cases are escalated to human specialists for review.

Autonomy without governance leads to unacceptable risk in insurance. The true effectiveness of an AI agent rests equally on its intelligence and the rigor of the governance framework surrounding it.

Top AI Agent Use Cases in Insurance

Insurance organizations are transitioning from task-based automation toward AI-driven ecosystems. Instead of just speeding up tasks, modern AI agents help insurers manage complex workflows, improve decision-making, reduce costs, and enhance the customer experience across the policy lifecycle.

From claims management to fraud prevention, AI agents act as an operational layer, enabling faster execution, more accuracy, and scalable growth.

The table below highlights some of the most impactful AI agent applications currently transforming the insurance industry.

|

Use case |

What the AI agent does |

Primary business value |

|

Claims processing agents |

Analyze claims, assess damage, verify coverage, coordinate investigations, and route cases automatically |

Faster claims resolution, lower operational costs, improved claims accuracy |

|

Intelligent quote and sales agents |

Gather customer data, generate personalized quotes, guide applicants through purchase journeys |

Higher conversion rates, lower customer acquisition costs, increased digital sales |

|

24/7 agentic customer support |

Resolve customer requests, update policy information, assist with claims, and perform service actions autonomously |

Improved customer satisfaction, increased service availability, reduced support workload |

|

Hyper-personalized communication agents |

Generate contextual customer communications across claims, renewals, onboarding, and policy servicing |

Better customer experience, fewer complaints, stronger policyholder engagement |

| Fraud detection and investigation agents |

Investigate suspicious activity, analyze behavioral patterns, identify fraud networks, and support investigators |

Reduced fraud losses, improved detection accuracy, lower investigation costs |

Let’s look at several key use cases that illustrate how insurance providers are applying AI agents across critical business functions.

AI claims processing agents

Technology

Multi-agent AI ecosystems are transforming claims operations by enabling specialized agents to collaborate at every stage of the claims lifecycle. This enables targeted analysis, improved evidence review, dynamic fraud detection, and optimized communication between teams.

Unlike static workflows, these AI systems adapt continuously. They share contextual data, reassess evolving situations, and make dynamic decisions based on new evidence, which enhances flexibility and accuracy throughout claims processing.

Business result

The operational gains can be significant. For example, Aviva reported that its AI-enabled claims initiatives reduced handling times by up to 65%, while simultaneously improving operational efficiency and customer experience. AI-supported orchestration also contributed to substantial productivity improvements across claims operations.

For insurers processing thousands of claims daily, even moderate improvements in routing accuracy, triage speed, and workload allocation can translate into millions in annual savings, lower operational friction, and faster policyholder resolutions.

Risk

Claims adjudication involves legal interpretation, nuanced policy language, and ever-evolving fraud tactics. Without sufficient governance and oversight, AI systems may misinterpret coverage conditions, overlook critical evidence, or fail to identify sophisticated fraudulent activity.

Best fit

Large insurance organizations managing high-volume claims operations across auto, property, health, travel, or commercial insurance portfolios.

Intelligent quote and sales automation agents

Technology

AI sales and quotation agents redefine the acquisition journey. By collecting real-time customer data, personalizing recommendations, and guiding applicants through each step, they empower insurers to deliver a seamless, responsive experience from inquiry to purchase.

Unlike conventional digital forms or scripted sales funnels, these agents adapt dynamically to customer intent, browsing behavior, demographic signals, and purchasing preferences throughout the interaction.

Business result

By reducing friction during the purchasing process, insurers can improve digital conversion rates while lowering acquisition costs. Some digital-first insurers report that nearly 80% of transactions are now completed entirely online, while customer advocacy indicators, such as Net Promoter Score (NPS) and referral metrics, have improved by as much as 36% through more personalized and intuitive purchasing experiences.

Risk

Incomplete or inaccurate customer data, weak system integrations, or flawed risk-evaluation logic may result in incorrect premium calculations, underwriting exposure, or interrupted purchase journeys, which can negatively affect conversion rates and profitability.

Best fit

Growth-focused insurers that invest in digital distribution, self-service purchasing experiences, and customer acquisition cost (CAC) optimization.

24/7 agentic customer support

Technology

Agentic support systems represent a major shift from traditional chatbots, as they perform operational tasks on behalf of customers. These agents verify policy information, update records, initiate claims, escalate important cases, and provide proactive 24/7 assistance.

Because these systems integrate directly with operational insurance platforms, they can autonomously resolve many customer requests instead of merely answering questions.

Business result

Always-available service environments improve responsiveness, accessibility, and customer convenience. Insurers can efficiently process inquiries during evenings and weekends, and across multiple time zones, without compromising service quality.

Some organizations have reported an 11% increase in new client acquisition due to improved traffic handling during nights and weekends, when prospective customers increasingly expect immediate digital engagement.

Risk

Incorrect explanations regarding policy coverage, exclusions, or claims procedures may expose insurers to reputational, regulatory, and financial liabilities.

Best fit

Global insurers, digital-native carriers, and organizations supporting customers who expect immediate assistance regardless of geography or operating hours.

Hyper-personalized communication agents

Technology

Generative AI communication agents directly enhance customer engagement by enabling insurers to deliver personalized communications–at scale–tailored to renewals, onboarding, claims updates, and service campaigns.

Instead of rigid templates, these systems adjust tone, structure, style, and details based on profiles, policy history, preferences, and claim circumstances.

Business result

Clearer and more contextual communication improves customer understanding, reduces service friction, and strengthens engagement throughout the policy lifecycle.

Some insurers have reported up to a 65% reduction in customer complaints after implementing AI-driven communication systems capable of generating up to 50,000 highly personalized messages per day. In many cases, customers perceived these interactions as more natural, understandable, and human-like than manually written communications.

Risk

Insufficient oversight may result in inaccurate messaging, inappropriate tone, inconsistent policy explanations, or communications that create legal or contractual ambiguity.

Best fit

Insurers seeking to strengthen customer experience, improve retention, and reduce pressure on service centers and support teams.

AI fraud detection and investigation agents

Technology

Fraud investigation agents serve as digital investigators, actively synthesizing and analyzing data from multiple sources to detect and prevent fraudulent activity, making fraud detection smarter and faster.

These systems may:

- Analyze relationships between claims participants.

- Detect abnormal behavioral patterns.

- Validate image metadata and supporting documentation.

- Monitor public and third-party information sources.

- Identify coordinated fraud networks.

- Surface anomalies requiring human investigation.

Unlike rule-based fraud engines, agentic systems continuously adapt to emerging fraud strategies and evolving criminal behaviors.

Business result

Earlier identification of suspicious activity allows insurers to reduce fraudulent payouts, improve investigative efficiency, and minimize false positives that disrupt legitimate claims.

Advanced AI-driven fraud systems are particularly effective at uncovering organized fraud rings and complex multi-party schemes that would be difficult to detect through manual investigation alone.

Risk

Overly aggressive detection models may delay legitimate claims, introduce unintended bias, or negatively affect customer trust and regulatory compliance.

Best fit

Auto, health, property, and specialty insurers seeking to strengthen fraud-prevention capabilities without proportionally expanding investigative teams.

Trust Architecture: How to Control Insurance AI Agents

Trust is now as crucial as capability for insurance AI agents. As automation expands in underwriting, claims, and compliance, these systems must remain transparent, secure, and operate within strict regulatory boundaries to earn and maintain trust.

A robust trust architecture helps organizations balance operational autonomy with accountability. Rather than granting AI agents unrestricted authority, insurers should establish governance frameworks that clearly define decision rights, escalation paths, auditability requirements, and oversight responsibilities.

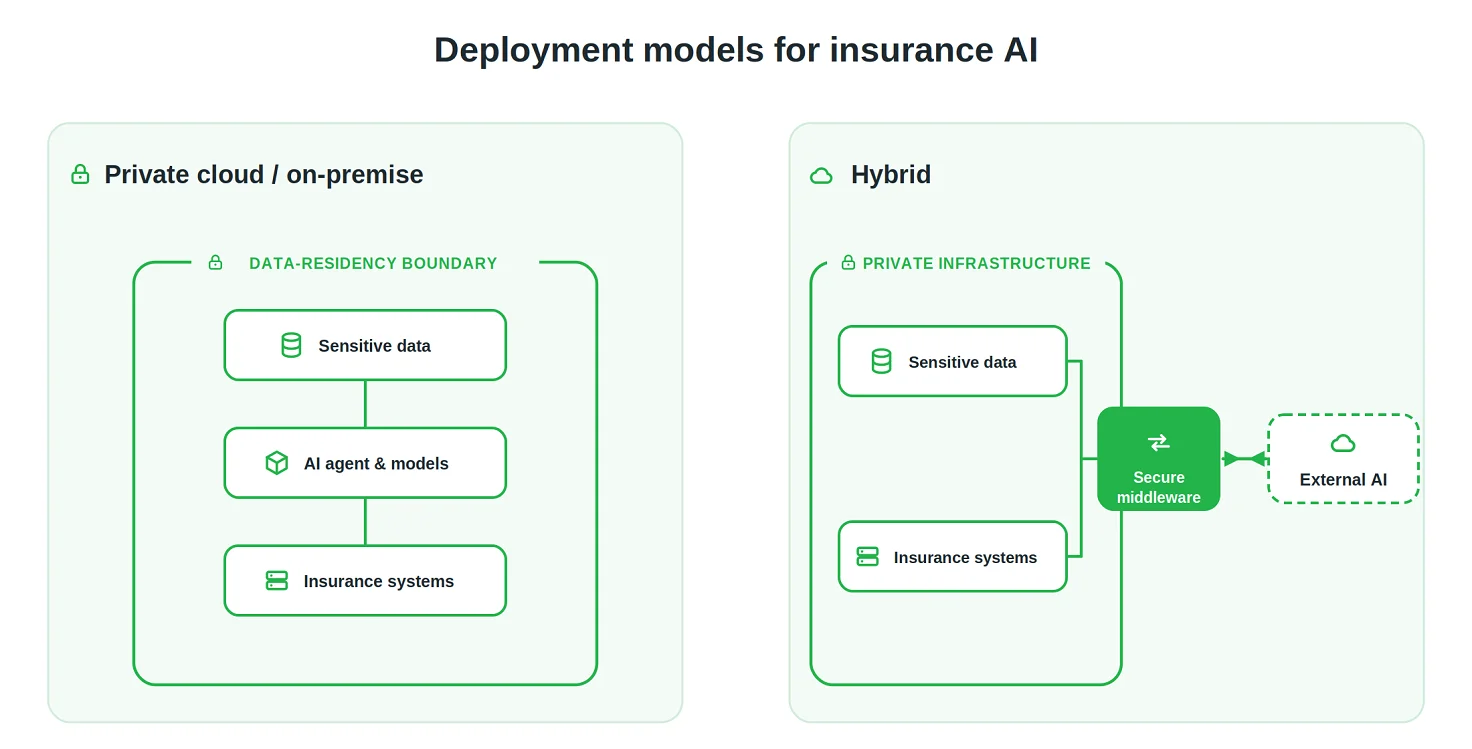

Deployment strategy: security and data sovereignty

Trustworthy AI in insurance starts with secure deployment. Handling sensitive data requires robust privacy controls, strong governance, and careful data residency to ensure compliance and customer trust.

Private cloud/on-premise deployment

Private cloud and on-premise environments provide insurers with the highest degree of operational control over sensitive data and AI infrastructure. This approach allows organizations to:

- Retain customer and claims data within controlled internal environments.

- Comply with strict regulatory and data residency obligations.

- Apply organization-specific cybersecurity policies.

- Minimize exposure to external AI providers.

- Maintain full visibility into system access and infrastructure activity.

This deployment model is particularly important for life, health, and heavily regulated insurance sectors.

Hybrid deployment models

Many insurers are adopting hybrid AI architectures that combine internal infrastructure with external AI services.

Within hybrid environments:

- Sensitive policyholder data remains inside private infrastructure.

- External AI services handle selected reasoning or content-generation tasks.

- Secure middleware governs information exchange between systems.

- Organizations gain flexibility without compromising compliance requirements.

For many insurers, hybrid models offer the most practical balance between scalability, innovation, operational efficiency, and regulatory control.

Audit trails and traceability (explainable AI)

Insurance decisions directly influence claims outcomes, pricing, fraud investigations, and regulatory reporting. As a result, AI-driven actions must remain explainable, reviewable, and fully auditable.

Decision trace logging

AI agents should document not only the actions taken, but also the reasons for those decisions.

A comprehensive decision trace may include:

- Consulted data sources

- Applied business rules and policies

- Intermediate analytical conclusions

- Confidence levels

- Executed actions

- Escalation or approval decisions

This visibility enables insurers to understand AI behavior, investigate operational outcomes, and more effectively satisfy compliance obligations.

Tamper-resistant audit logs

Every operational action performed by an AI agent should be immutably recorded.

Examples include:

- Claims status modifications

- Policy updates

- Customer communications

- Payment authorizations

- Fraud investigation activities

- CRM record changes

These records should remain protected from alteration and accessible for audits, compliance reviews, and internal investigations.

As regulatory scrutiny surrounding AI continues to increase, auditability is rapidly becoming a baseline operational requirement rather than a competitive differentiator.

Tiered autonomy and human-in-the-loop governance

Not every insurance workflow requires the same degree of AI autonomy. The table below presents a practical model that balances efficiency with human oversight and regulatory accountability.

| Autonomy level | What the agent can do | Example use case | Human control |

| Suggest | Generates recommendations, summaries, or draft responses without taking action. | Drafting a response to a customer complaint or generating an underwriting recommendation. | A human reviews, edits, and approves the output before it is sent or used. |

| Prepare | Collects information, performs research, and prepares the next step in a workflow. | Gathering data from internal and external sources to support an underwriting assessment. | An employee verifies data completeness and accuracy before proceeding. |

| Act with review | Executes predefined actions but requires explicit approval before completion. | Calculating a standard claims settlement amount and preparing payment instructions. | A claims specialist reviews the recommendation and approves the action. |

|

Act autonomously |

Performs low-risk actions independently within predefined operational boundaries. | Sending policy renewal reminders, processing routine policy updates, or handling low-value claims below a defined threshold. | Human supervisors monitor system performance, KPIs, and exception reports. |

| Stop and escalate | Detects risk indicators and pauses workflow execution until a human intervenes. | Identifying potential fraud, compliance concerns, suspicious transactions, or policy conflicts. | A qualified expert assumes responsibility for reviewing and resolving the case. |

Routine administrative activities may be handled autonomously, whereas high-risk underwriting decisions, complex claims approvals, fraud investigations, and compliance-sensitive cases should still involve human review and escalation mechanisms.

This layered approach allows insurers to responsibly scale AI while preserving transparency, accountability, operational control, and customer trust.

What Can Go Wrong? Key Risks of Insurance AI Agents

As AI agents become integral to underwriting, claims, and customer service, insurers face a core challenge: balancing efficiency gains with robust oversight. The growing reliance on agentic systems promises a major competitive advantage, but introduces critical risks—operational, regulatory, and technological. Framing and addressing these risks early is essential to create insurance AI that is not just innovative but also reliable, compliant, and scalable.

Regulatory and compliance risk

Insurance is one of the most regulated sectors, and any AI-driven system must navigate complex, jurisdiction-specific legal frameworks. Whether supporting underwriting, processing claims, or handling data, AI agents must operate strictly within regulatory boundaries.

Without robust governance, systems may breach consumer protection, privacy, or new AI rules. Small deviations can lead to fines, scrutiny, reputational damage, or lost trust. The challenge is not only meeting today’s standards, but also keeping pace with evolving regulations.

Decision errors and hallucinations

Although AI agents are designed to reason, interpret, and execute tasks, they are not immune to inaccuracies, incomplete reasoning, or misleading outputs.

In insurance workflows, even minor mistakes can have sizable consequences. Incorrect risk classification, flawed claim evaluation, or misinterpretation of policy terms can result in financial losses, disputes, and operational disruption.

To counter this, insurers use safeguards like confidence scoring, validation, and structured human review to verify critical decisions.

Bias and fairness concerns

Insurance decisions affect pricing, eligibility, claims, and experience. If training data is biased, AI can reinforce unfair results. This creates risks of discrimination, unequal treatment, and regulatory scrutiny. As transparency expectations rise, insurers face more pressure to audit decisions for fairness.

Responsible AI governance is becoming a competitive differentiator, not just a compliance obligation.

Data security and systemic dependency risk

AI agents in insurance handle sensitive data, making them targets for cyber threats. As they become central to operations, security breaches have a greater impact. Beyond cybersecurity concerns, there is also the issue of systemic dependency. When business-critical workflows rely heavily on AI, outages, malfunctions, or degraded performance can disrupt multiple operational areas simultaneously.

To address these, insurers must build resilient infrastructure, enforce strong access controls and cybersecurity, and maintain disaster recovery plans. The goal is to embed AI within the same governance and rigor as other mission-critical systems.

The Future of AI Agents in Insurance: Key Trends

Insurance is moving from isolated automation to AI-enabled ecosystems. AI agents will evolve from task assistants to orchestration layers managing entire insurance lifecycles. Research, including KPMG insights, shows a shift to intelligent models where data, automation, and decisions converge. Key trends shape this transformation.

End-to-end autonomous insurance operations

Current insurance workflows still depend on manual coordination. In the future, AI systems will manage full journeys across issuance, underwriting, claims, and service.

While human oversight will remain, insurers will increasingly delegate entire operational chains to AI systems. This is likely to reduce friction, improve consistency, and significantly accelerate decision-making.

Real-time, dynamic, and event-driven insurance

Traditional models rely on periodic reviews and static policies. AI agents enable event-driven systems that respond to real-time changes.

Data from connected devices and contextual signals enable insurers to adjust risk, claims, and support in real time. This shift moves processes from reactive to proactive risk management.

Continuous underwriting and adaptive pricing

Underwriting has been tied to fixed points, such as policy issuance or renewal. With AI, this model now evolves continuously.

Risk profiles can be updated dynamically based on behavioral changes, environmental factors, and incoming data streams. This supports more precise pricing, improved risk selection, faster policy adjustments, and more tailored coverage.

Multi-agent insurance ecosystems

The future of insurance involves networks of specialized AI agents, not single central systems.

Different agents will focus on distinct responsibilities, including underwriting analysis, fraud detection, claims processing, customer communication, compliance monitoring, and policy servicing. Working within shared frameworks, these agents will coordinate actions under unified governance structures. This distributed model boosts scalability, resilience, and specialization, letting insurers expand AI without rebuilding systems.

AI agents are intended to augment, not replace, human expertise. The future is controlled autonomy, where intelligent systems work within clear boundaries, are transparently monitored, and accountable to human decision-makers.

Conclusion

AI agents are fundamentally reshaping insurance by moving automation from isolated tasks to integrated workflows. Their adoption in claims, underwriting, and customer interactions unlocks efficiency, faster decisions, and enhanced customer outcomes, but requires a careful balance between opportunity and risk.

Capturing these benefits requires mindful governance, transparent decision-making processes, rigorous security measures, and durable human oversight for scalable, long-term impact.

If you're exploring AI agents for insurance and looking for a trusted AI technology partner, Emerline can help you design, develop, and scale secure, enterprise-grade AI solutions tailored to your business objectives. Contact us to evaluate your opportunities, define the right AI strategy, and build insurance solutions that deliver measurable business results.

Published on Jun 11, 2026