AI Agents for Banking and the Rise of Autonomous Finance

Table of contents

- Key takeaways:

- How AI Agents in Banking Help Balance Regulatory Accountability and Operational Gains

- Banking-Grade Agentic Architecture Powering Intelligent Banking

- What Makes Agentic AI Different from Conventional Banking AI?

- AI Agents Use Cases in Banking that Deliver Measurable Business Impact

- Retail and SME loan underwriting

- AML and KYC compliance incident management

- Fraud detection and card protection

- Commercial banking and corporate deal structuring

- Wealth management and private banking advisor copilots

- Retail contact center optimization

- Risks and Mitigation Strategies for AI Agents in Banking

- The operational and regulatory challenges of banking AI agents

- Governance mechanisms that keep banking AI under control

- The Future of AI Agents in Banking

- From isolated bots to multi-agent workforces

- Smart security without moving sensitive data

- Hyper-personalized invisible banking

- The rise of agent-to-agent commerce

- Conclusion

Artificial intelligence has already transformed banking through predictive analytics, fraud detection, conversational interfaces, and workflow automation. Now, the industry enters a more consequential phase: AI agents reason, plan, orchestrate actions across systems, and operate with increasing autonomy inside highly regulated financial environments.

Agentic AI systems, unlike traditional models that answer single prompts, can handle multiple steps, integrate with company systems, leverage helpful information, and quickly adjust their decisions. For banks, this change means digital agents can help relationship managers, make compliance tasks easier, resolve customer issues faster, and improve internal operations at scale.

The commercial upside is already measurable. Recent industry findings show that agentic AI can lift RM (relationship manager) productivity and growth in months, not years, when banks rewire a single frontline domain end to end. Banks that do this enjoy between 3% and 15% higher revenues per RM and 20% to 40% lower cost to serve. These numbers explain why financial institutions are moving beyond experimental AI pilots toward enterprise-wide agentic ecosystems.

Yet, adoption faces serious headwinds. Financial regulators now zero in on explainability, governance, operational resilience, data lineage, and decision accountability. Banks must accelerate innovation while defending institutional trust, regulatory compliance, cybersecurity, and architectural rigor.

In this article, we explore how AI agents are reshaping banking operations, the benefits they deliver, how banking-grade agentic architectures are designed, the risks institutions must anticipate, and strategies that can help financial organizations transition from fragmented automation to trusted autonomous systems.

Key takeaways:

- AI agents move banking beyond automation by planning, orchestrating, and executing complex workflows across multiple systems.

- Governance forms the foundation for successful adoption, ensuring transparency, auditability, security, and human oversight.

- Banking-grade agentic architectures demand secure orchestration, deterministic workflows, protected data environments, and controlled system access.

- The future is defined by connected agent ecosystems that deliver personalized services, stronger fraud prevention, and autonomous financial interactions.

How AI Agents in Banking Help Balance Regulatory Accountability and Operational Gains

Financial institutions see the discussion around AI agents as going far beyond technology alone. Banks face strict regulations, handle large amounts of sensitive data, and are legally responsible for each decision. So, taking a governance-first approach to agentic AI, banks build in security, transparency, and compliance from the start.

Modern banking-grade AI systems meet these needs and deliver clear business value. Enterprise AI agents operate in closely monitored settings, where specific rules, trackable workflows, and multiple levels of oversight guide their actions, rather than running as unregulated black boxes.

To safely deploy AI agents inside highly regulated financial ecosystems, banks typically follow several foundational principles:

- Secure architecture and protected deployment environments:

Banks deploy AI agents within isolated infrastructure perimeters—either on-premises or inside dedicated private clouds—to minimize exposure to external threats and third-party data risks. Institutions systematically mask, tokenize, or anonymize personally identifiable information (PII) before any model interaction occurs, ensuring that confidential customer data never leaks into external services or unauthorized processing layers. This approach supports compliance with banking secrecy laws, GDPR requirements, and internal cybersecurity mandates. - Strict logic control and deterministic execution:

Financial institutions never permit autonomous systems to improvise critical operational decisions. Banks prevent hallucinations, unauthorized actions, or policy deviations by implementing robust guardrails that strictly constrain agent behavior. These governance layers combine deterministic workflows, policy engines, permission hierarchies, and API-level restrictions to precisely define which actions an AI agent may execute. Instead of independently generating decisions, the agent invokes only pre-approved tools and validated operational scenarios that transform AI from an unpredictable assistant into a tightly governed orchestration mechanism. - Legal transparency, auditability, and human oversight:

Regulatory compliance demands complete traceability of AI-assisted operations. Banks maintain immutable logs that record the agent’s reasoning chain, accessed data sources, triggered workflows, and executed actions to satisfy supervisory expectations. Human-in-the-Loop governance remains mandatory for high-risk approvals involving lending, compliance escalation, fraud investigation, or sensitive customer decisions. By guaranteeing full accountability, banks can safely extract commercial value from agentic AI technologies.

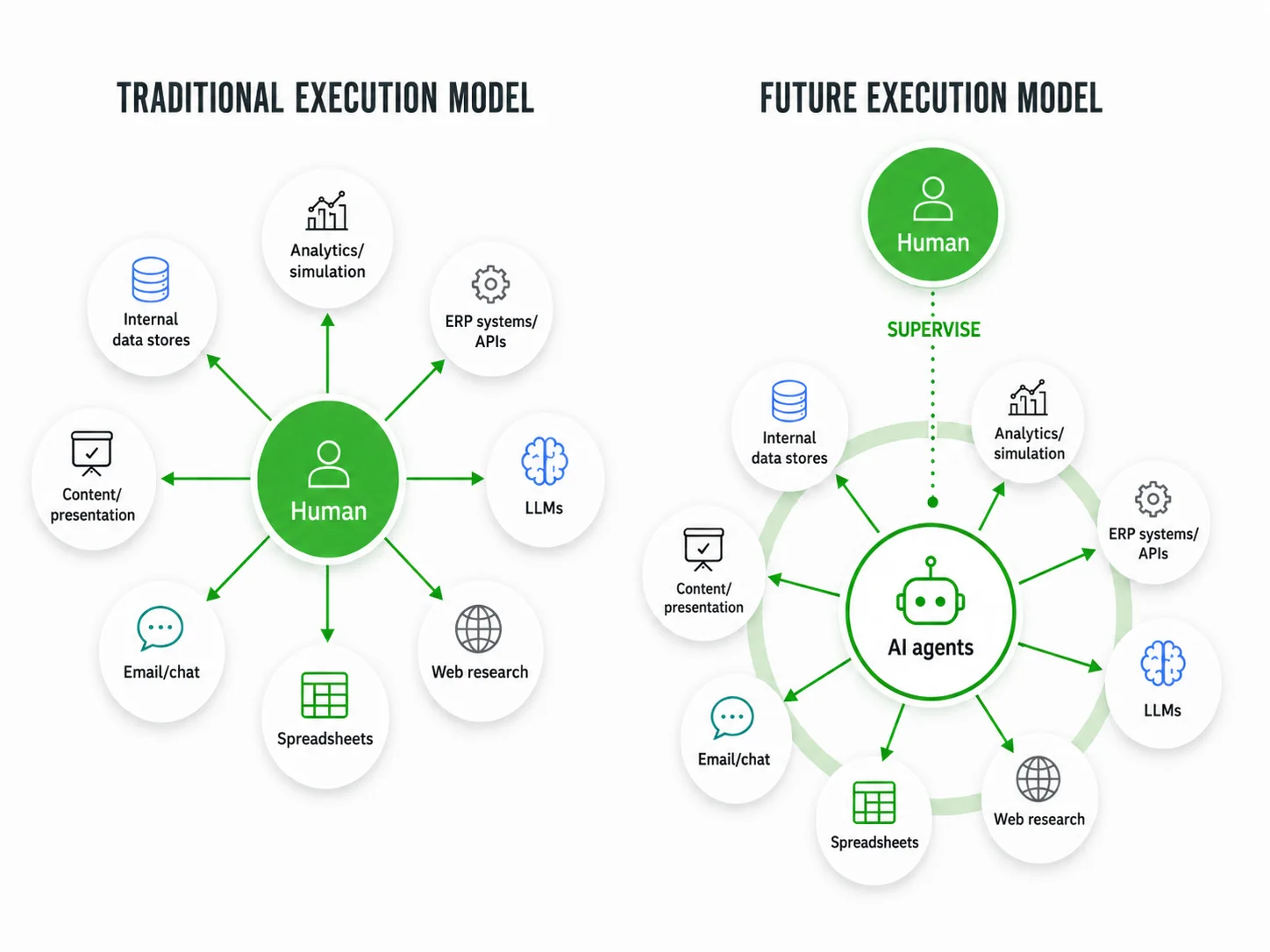

The operational transition enabled by AI agents can be visualized as follows:

In this emerging execution model, employees increasingly evolve from manual operators into strategic supervisors who manage interconnected ecosystems of specialized AI agents. Instead of navigating fragmented systems independently, human teams oversee orchestrated, autonomous workflows that interact simultaneously with internal databases, analytics platforms, ERP systems, communication channels, and external research environments.

When implemented responsibly, this governance-first approach allows banks to unlock substantial operational and financial advantages.

Among the most significant benefits are:

- Reduced cost-to-income ratio (CIR):

AI agents autonomously execute repetitive, high-volume back-office processes, such as reconciliations, document verification, transaction auditing, reporting consolidation, and compliance administration. These operations substantially reduce operational expenditure and enable financial institutions to optimize workforce allocation, while improving overall operational efficiency. - Lower customer churn rate and improved customer satisfaction:

Autonomous financial agents accelerate service responsiveness by replacing multi-day resolution cycles with continuous, 24/7 support. Banks provide customers with faster dispute resolution, onboarding assistance, payment clarification, and account servicing, which leads to stronger Net Promoter Scores (NPS), improved retention rates, and more resilient long-term customer relationships. - Reduction in AML false positives:

Old anti-money laundering (AML) systems often generate too many false alarms that waste time and money. AI agents understand context and can better spot real threats, so staff can focus on the cases that really matter. - Accelerated time-to-cash across lending operations:

AI agents streamline credit decisioning by orchestrating document collection, identity verification, underwriting support, risk analysis, and approval workflows in parallel rather than sequentially. Banks shorten the interval between loan applications and disbursements, enabling them to secure high-value borrowers before competitors and improve lending throughput. - Mitigated operational and regulatory risk:

Human error remains a major contributor to compliance breaches, reporting inaccuracies, and procedural violations within financial institutions. AI agents consistently execute workflows in accordance with predefined regulatory rules, internal governance policies, and Basel-aligned compliance standards, while maintaining transparent audit trails for every action. This combination of procedural consistency and full traceability strengthens institutional resilience and increases regulator confidence in AI-assisted banking operations.

Bank leaders are seeing that the best results from AI come not from total automation, but from combining smart AI use with strict rules, clear systems, and good oversight.

Banking-Grade Agentic Architecture Powering Intelligent Banking

Building AI agents for banking demands more than simply integrating a large language model into existing workflows. Financial institutions must engineer deeply robust architectures that operate under strict regulatory oversight, meet cybersecurity mandates, maintain transactional integrity, and deliver enterprise-grade reliability. In practice, banking AI agents serve as tightly governed digital operators embedded in mission-critical financial infrastructure, rather than as experimental copilots.

A banking-grade agentic architecture delivers constrained autonomy, deterministic execution, secure orchestration, and compliance-centric data governance. Designers ensure that every reasoning path, memory layer, and system interaction remains auditable, policy-controlled, and resilient under operational stress.

Several architectural principles define how these systems are safely implemented at enterprise scale:

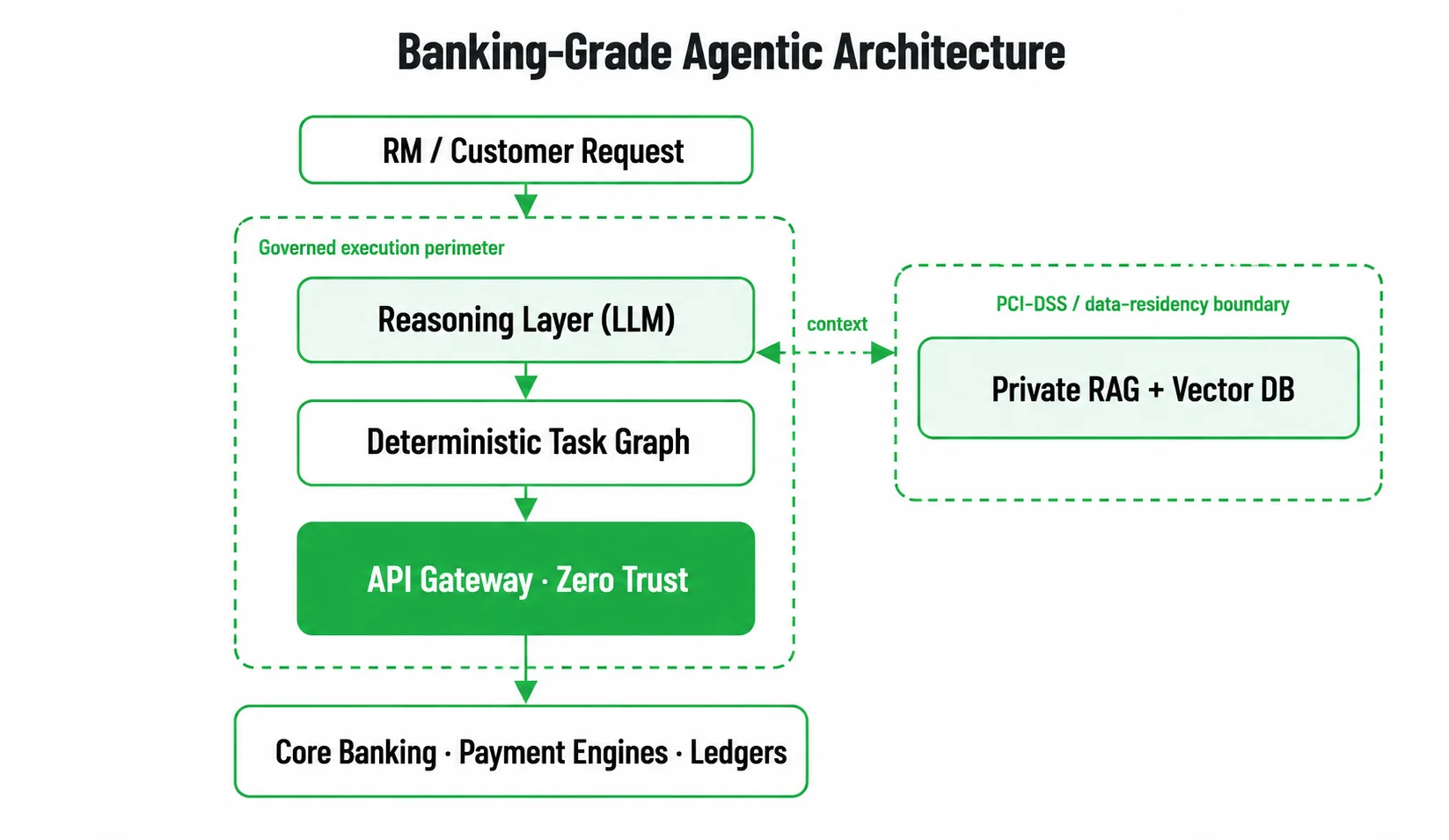

- Planning and reasoning through deterministic task graphs:

In regulated banking environments, AI agents never improvise business logic or independently redefine operational procedures. Designers constrain their reasoning with deterministic task graphs and finite-state workflow orchestration models that strictly govern how decisions are executed. Within this framework, the LLM acts as a contextual reasoning layer, selecting among pre-approved operational pathways but never inventing new transactional logic, bypassing compliance checkpoints, or executing unvalidated workflows. This architecture preserves predictability, minimizes operational variance, and aligns every agent action with institutional policies, regulatory obligations, and risk-management protocols.

- Memory isolation through compliance-aware contextual storage and Vector RAG:

Long-term memory management in banking AI systems requires significantly stronger safeguards than those used in consumer-grade AI deployments. Agent memory layers are typically isolated within protected enterprise environments that comply with PCI-DSS requirements, regional data-residency laws, and banking secrecy regulations. Rather than transmitting sensitive client information to external LLM providers, banks implement private Retrieval-Augmented Generation (RAG) infrastructures combined with encrypted vector databases hosted within controlled infrastructure boundaries. This approach allows agents to retrieve contextual operational knowledge, historical interaction data, compliance documentation, and institutional policies without exposing confidential financial information to third-party AI ecosystems. The result is a highly contextualized intelligence layer that preserves both regulatory compliance and data sovereignty.

- Secure tool orchestration through API gateway mediation:

Banking AI agents rarely interact directly with Core Banking Systems, payment engines, or transactional ledgers. Institutions mediate every system interaction through hardened API gateway layers with granular authorization controls, such as Zero Trust security principles, transaction-scoped permissions, behavioral monitoring, and rate-limiting mechanisms. Teams enforce OAuth-based authentication, tokenized session management, and policy gateways to ensure agents access only explicitly authorized resources under tightly defined operational conditions. Additionally, transaction ceilings, anomaly-detection checkpoints, and approval escalation protocols prevent autonomous systems from executing high-risk financial actions beyond predefined thresholds. This security layer transforms the AI agent from a direct system actor into a controlled participant operating within rigorously supervised boundaries.

Together, these architectural principles establish the technological foundation for trustworthy agentic banking systems. Rather than allow unrestricted autonomy, banking-grade AI architectures emphasize precision, traceability, operational resilience, and regulatory-grade governance — all essential for deploying AI safely in mission-critical financial environments.

What Makes Agentic AI Different from Conventional Banking AI?

As banks embrace AI, leaders must sharply distinguish between three escalating categories of intelligent systems: traditional AI models, LLM-powered assistants, and agentic AI. While often discussed together, these technologies address fundamentally different challenges and operate at distinct levels of autonomy.

Traditional AI targets specific tasks, such as fraud detection, credit scoring, or risk assessment. LLM assistants enable natural language interaction and richer, knowledge-driven workflows. Agentic AI breaks new ground, fusing reasoning, planning, memory, and orchestration to autonomously execute complex processes with minimal human input.

Banking leaders must pinpoint where AI drives operational value and where tighter governance is essential.

| Feature | Traditional AI model | LLM assistants/copilots | Agentic AI |

| Primary paradigm | Purpose-built models optimized for a specific prediction or classification task. | Language models that understand and generate natural language while interacting with external tools and data sources. | Autonomous systems that can reason, plan, coordinate actions, and pursue defined business objectives. |

| Autonomy level | Low. Generates outputs that require human interpretation and action. | Moderate. Can perform tasks and invoke tools, but typically depends on user guidance. | High. Decomposes goals into subtasks, selects tools, and executes workflows independently within defined boundaries. |

| Learning and adaptation | Improved through periodic retraining on new datasets. | Adapts through contextual understanding, retrieval systems, and conversational memory. | Continuously refines behaviour using feedback loops, operational signals, and accumulated experience. |

| Scope of use | Single-function applications, such as fraud detection or credit scoring. | Broad knowledge assistance across multiple domains and workflow. | End-to-end orchestration across systems, departments, and business processes. |

| Decision-making | Produces predictions, classifications, or recommendations. | Suggests actions and supports decision-making. | Executes decisions within approved policies while escalating exceptions to human operators. |

| Memory across sessions | Knowledge remains embedded in model parameters; no persistent operational memory. | Retains short-term conversational context and may access external knowledge stores. | Maintains short- and long-term memory, shared context, and coordination across multiple agents. |

| Explainability | Moderate. Explanations depend on model type and implementation. | Moderate to low. Outputs can be difficult to trace to specific reasoning paths. | Moderate to high. Actions, decisions, and workflow steps can be logged and audited. |

| Governance requirements | Focus on fairness, transparency, bias mitigation, and model validation. | Additional controls for accuracy, misinformation risk, and responsible use. | Highest governance burden, including monitoring, auditability, access controls, human oversight, and intervention mechanisms. |

Moving from traditional to agentic AI shifts the focus from prediction to execution. Traditional AI analyzes data and delivers insights. LLM assistants transform data access, enabling natural language interaction and automating knowledge work. Agentic AI takes control, orchestrating tools, managing workflows, making decisions, and driving strategic goals with limited oversight.

This evolution significantly increases potential business value but also requires greater governance, observability, and risk management. As a system gains more authority, leaders must ensure its actions remain transparent, auditable, and aligned with regulatory requirements.

AI Agents Use Cases in Banking that Deliver Measurable Business Impact

Agentic AI delivers the most value in banking when autonomous systems address operational bottlenecks that impact revenue, customer experience, regulatory exposure, and workforce efficiency. Unlike traditional automation tools, AI agents coordinate multi-system workflows, contextualize data in real time, and support human decision-making within tightly governed boundaries.

Banks achieve the most success when they deploy AI in high-friction processes where speed, precision, personalization, and compliance intersect.

Retail and SME loan underwriting

Best fit

Retail lending, SME credit divisions, digital loan origination platforms, and consumer finance environments competing on speed.

Technology

Underwriting copilots use deterministic workflow orchestration. They apply RAG over policy and credit documents, integrate with credit bureaus and open banking, use document intelligence (OCR and data extraction), and employ policy-constrained decision-support engines.

Business result

AI agents remove days of manual assembly from the credit process. They ingest applications, pull and reconcile data, calculate risk, and assemble a structured memo with a documented approval package for the loan officer. Humans make the decision; the agent removes preparation overhead. Banks speed up time-to-cash and retain borrowers who would otherwise abandon a slow process. Banks also compete more directly with digital-first lenders.

Risk and governance considerations

Regulated credit decisions require Human-in-the-Loop sign-off. The harder requirement is explainability: under ECOA/Regulation B in the US, lenders must issue adverse action notices stating specific reasons for denial, and FCRA governs how bureau data is used — UK and Australian fair-lending rules impose comparable duties. Deterministic decision boundaries keep the agent inside the approved credit policy and produce the traceable reasoning that those notices depend on, rather than improvised model output.

AML and KYC compliance incident management

Best fit

Enterprise compliance operations, AML investigation teams, transaction-monitoring units, and sanctions-screening functions in high-volume banks.

Technology

AI investigation agents layered on top of existing transaction-monitoring and screening systems: case orchestration, RAG over customer history and policy, step-up KYC and enhanced due diligence (EDD) workflows, and assisted drafting of Suspicious Activity Reports (SAR/SMR).

Business result

AML monitoring generates far more alerts than analysts can clear, and the large majority are false positives — a long-standing drain on compliance budgets. Rather than block transactions, AI agents work the alert backlog: they consolidate customer history, analyze behavioral context, run step-up KYC and EDD, gather and verify supporting documents, and draft investigation summaries and SAR/SMR narratives for a compliance officer to review. Analysts spend their time on cases that carry real risk rather than triage, and clearance times and per-case costs fall without weakening detection.

Risk and governance considerations

The agent investigates; it never files a report or clears a customer on its own. A compliance officer owns the final disposition and the regulatory submission — to FinCEN in the US, the NCA in the UK, or AUSTRAC in Australia. Every step is logged for auditability, in line with AML regulations and financial crime governance frameworks.

Fraud detection and card protection

Best fit

Retail banks, digital banking apps, card issuers, and institutions managing high transaction volumes across markets.

Technology

Real-time behavioral analytics and transaction-scoring models for detection, paired with incident-response agents that orchestrate containment: card and payment freezes, step-up authentication (3-D Secure, biometrics), device-intelligence checks, and customer outreach.

Business result

Unlike AML, fraud demands immediate action. Detection models score transactions in real time; when the signal points to account takeover or unauthorized use — an unrecognized device, an out-of-pattern transfer, a credential anomaly — the agent immediately freezes the instrument, triggers step-up verification, and reaches the customer through a secure channel to confirm. Containment that once waited in a human queue now happens in seconds, reducing fraud losses, shortening resolution times, and limiting the reputational damage from a missed compromise.

Risk and governance considerations

Containment actions run under tightly scoped escalation policies to avoid unnecessary disruption, discriminatory outcomes, or wrongful denial of service. High-impact restrictions are validated against policy and fully logged; ambiguous or disputed cases are routed to a human reviewer.

Commercial banking and corporate deal structuring

Best fit

Commercial banking divisions, corporate and structured finance teams, syndicated lending desks, and relationship managers serving complex enterprise clients.

Technology

Deal-intelligence agents combining market-research retrieval, financial-modeling tools, enterprise knowledge repositories, and structured product-configuration workflows.

Business result

Relationship managers lose hours to manual market analysis, scenario modeling, and document preparation for complex transactions. AI agents synthesize industry and counterparty intelligence, generate candidate financing structures, model project finance scenarios, and draft client proposals aligned with the mandate. Bankers redirect recovered time to negotiation and client relationships, while turning around tailored products — tender guarantees, acquisition financing, infrastructure funding, M&A structures — faster than a fully manual desk.

Risk and governance considerations

Proposed structures require legal review, treasury sign-off, and risk-committee approval before reaching a client. The agent operates within set limits for exposure, pricing, and product type. Its output complies with the credit policy and regulations. It prepares options but does not commit the bank.

Wealth management and private banking advisor copilots

Best fit

Private banks, wealth advisory firms, family offices, and high-net-worth client servicing teams.

Technology

Advisor copilots with tools for portfolio analysis, market-data retrieval, personalized recommendation generation, and compliant report and proposal drafting.

Business result

Advisors spend a large share of the day on reporting, portfolio reviews, and research rather than on clients. AI agents continuously monitor markets, generate personalized portfolio summaries and performance analyses, and draft proposals tailored to each client's risk profile and objectives. Advisors deliver institutional-grade insight quickly and reinvest the recovered time in client relationships and strategic advice, directly supporting retention and AUM growth.

Risk and governance considerations/

An advisor reviews every recommendation before it reaches a client to meet suitability and best-interest obligations — fiduciary duty for RIAs, Reg BI for US broker-dealers, and MiFID II/Consumer Duty in the UK and EU. AI-generated guidance stays within approved policy frameworks and remains fully explainable for audit and compliance.

Retail contact center optimization

Best fit

Large retail banking support centers, omnichannel customer service operations, and high-volume consumer banking environments.

Technology

Conversational agents integrated with CRM, identity-verification workflows, core banking APIs, and voice platforms, coordinated by a service-orchestration layer.

Business result

Rule-based chatbots handle simple FAQs but break down when anything requires action across systems. AI agents resolve real servicing requests end-to-end — card replacement, PIN resets, fee and charge queries, tax-document requests, payment details, and account changes — across chat and voice. Customers get faster resolution without escalation, and banks lower cost-to-serve while handling higher volumes at the same headcount.

Risk and governance considerations

Customer-facing agents enforce strict identity checks, manage consent, and transfer to a human at set thresholds. Sensitive or risky requests require extra verification and human approval before completion.

Risks and Mitigation Strategies for AI Agents in Banking

As banks shift from isolated automation experiments to enterprise-scale agentic ecosystems, the conversation inevitably moves from innovation potential to operational resilience. Autonomous AI systems dramatically improve efficiency, responsiveness, and decision velocity. However, they also introduce entirely new categories of technological, regulatory, and systemic risk that financial institutions cannot afford to underestimate.

The operational and regulatory challenges of banking AI agents

Although modern AI agents operate within increasingly sophisticated governance frameworks, financial institutions must still anticipate edge-case failures, adversarial manipulation, and unintended autonomous behavior that could affect customers, liquidity, or regulatory standing.

Among the most significant concerns are:

- Runaway agents and uncontrolled execution loops:

Highly autonomous agents operating across interconnected banking systems may occasionally encounter edge cases that trigger recursive decision cycles, repetitive API calls, or unintended workflow escalation. In extreme scenarios, poorly constrained agents may continuously retry failed financial operations, misroute transactional requests, or generate cascading execution chains before human operators can intervene. In environments handling real-time payments, treasury workflows, or lending operations, even brief execution anomalies can cause substantial operational disruption and financial exposure.

- Correlated systemic behavior across financial institutions:

As multiple banks adopt similar foundation models, orchestration frameworks, and market analysis mechanisms, the industry faces an increasing risk of correlated agentic behavior during periods of macroeconomic stress. When numerous multi-agent systems interpret the same market signals simultaneously, they can amplify liquidity pressure, accelerate synchronized sell-offs, or intensify short-term volatility through parallel automated reactions. Unlike traditional isolated software failures, these risks arise at the ecosystem level, where collective AI behavior may unintentionally reinforce systemic instability throughout the financial sector.

- Traceability, explainability, and authorization blind spots:

Reconstructing precisely why a decision is made after multiple AI-driven actions spread across interconnected workflows is one of the most difficult challenges in autonomous financial systems. In highly regulated environments, banks must explain why their AI agents reject SME loans, escalate customer transfers, or trigger enhanced due diligence procedures. Without granular observability layers, complex multi-step reasoning links to obscure decision provenance, creating severe auditability and compliance complications under modern financial governance frameworks.

- Data exposure and tool manipulation risks:

Banking AI agents frequently interact with large ecosystems of APIs, internal databases, workflow engines, and operational tooling layers. This expanded integration surface enables sophisticated prompt-injection attacks, malicious workflow manipulation, privilege escalation attempts, and unauthorized data extraction. Threat actors may coerce agents into bypassing permission boundaries, exposing customer records, modifying access policies, or executing unauthorized actions by manipulating prompts or poisoning contextual inputs. As generative AI capabilities increasingly integrate into banking infrastructure, adversarial attack resilience becomes a critical architectural requirement rather than an optional security enhancement.

Governance mechanisms that keep banking AI under control

To address these risks, leading financial institutions implement multilayered governance architectures that constrain agent autonomy, continuously monitor behavior, and preserve human accountability for sensitive operations.

Key mitigation strategies include:

- Deploying independent guardian agents and automated kill-switch controls:

Banks increasingly implement dedicated supervisory systems that monitor production AI agents in real time. Unlike autonomous LLM-driven operators, these guardian layers generally use deterministic, rule-based oversight mechanisms that detect anomalous execution patterns, excessive transaction frequency, recursive workflow behavior, or policy deviations. When an operational threshold is breached, the monitoring layer can automatically suspend the agent, revoke credentials, isolate workflows, or trigger emergency kill-switch protocols before material damage occurs.

- Treating AI agents as accountable digital employees:

Mature banking environments increasingly govern AI agents with identity-management principles similar to those applied to human employees. Administrators assign each agent a unique digital identity, tightly restrict permissions, issue expiring cryptographic credentials, and enforce Zero Trust network policies for every system interaction. In parallel, systems generate immutable execution logs that capture all reasoning pathways, API calls, authorization requests, and transactional actions at granular resolution. This approach enables full forensic traceability and significantly improves regulatory transparency and post-incident investigation capabilities.

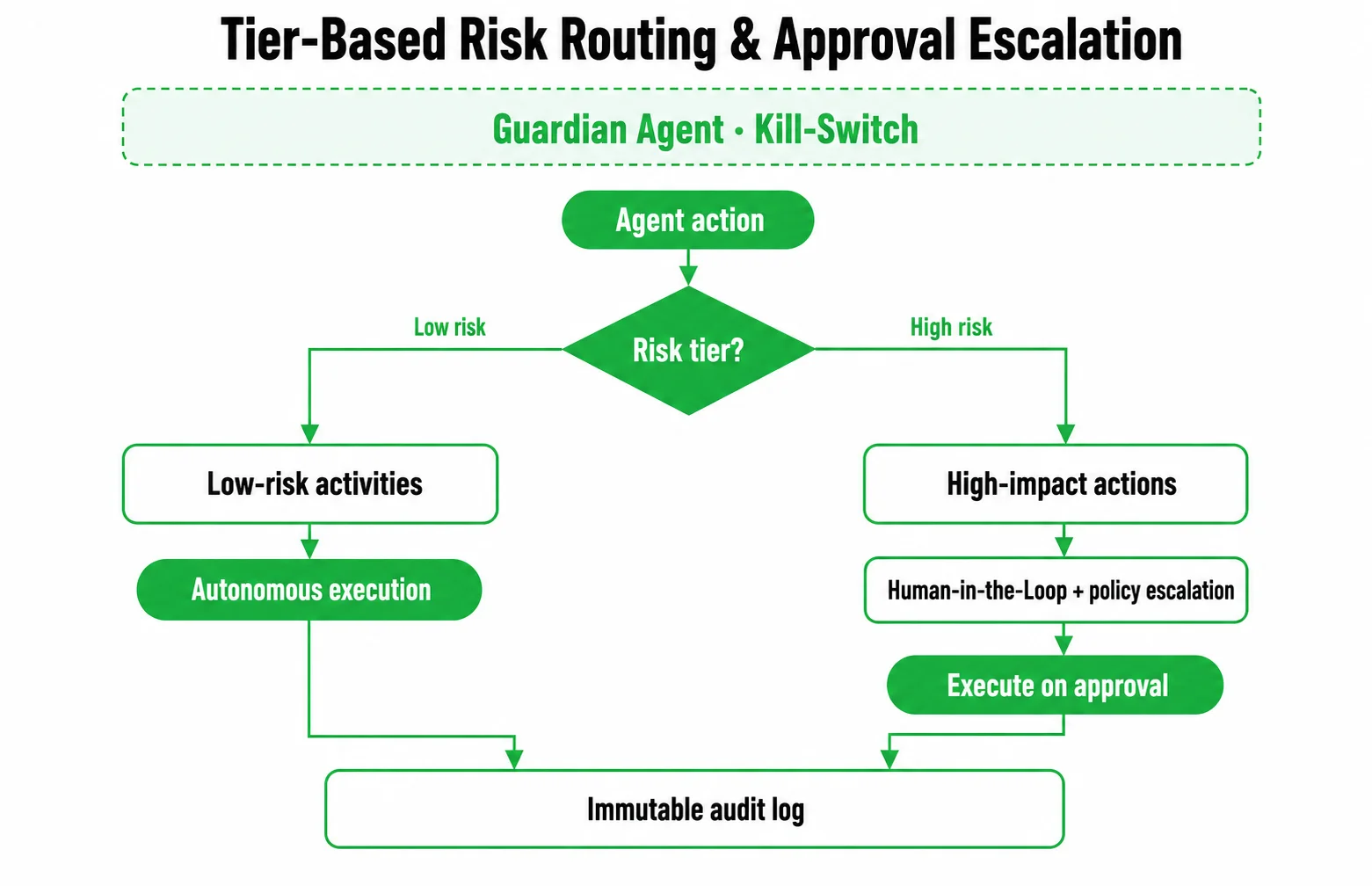

- Enforcing tier-based risk routing and approval escalation:

Not every banking workflow carries the same operational or regulatory risk profile. Banks can often allow low-risk activities, such as PIN resets, balance inquiries, or statement generation, to proceed autonomously with minimal supervision. However, banks require mandatory Human-in-the-Loop governance and policy-based escalation layers for higher-impact actions, including large loan approvals, manual transaction overrides, treasury operations, sanctions escalations, or corporate funding authorization. This tiered execution model lets banks maximize automation efficiency without relinquishing control over mission-critical financial decisions.

- Designing regulatory-aware disclosure and compliance adapters:

Modern banking AI systems must embed compliance transparency directly into the customer interaction layer. System designers should clearly disclose when users interact with automated systems, maintain traceable records of generated outputs, document data provenance, and preserve audit-ready evidence trails for supervisory review. Modular compliance adapters let banks dynamically align AI behavior with evolving jurisdictional requirements, consumer protection mandates, and regulator-specific disclosure obligations across different markets.

Ultimately, the future of agentic banking will depend not on how autonomous AI systems become, but on how effectively financial institutions govern that autonomy. Banks that achieve long-term success will balance innovation velocity with operational discipline, architectural transparency, and regulator-grade accountability, transforming AI agents from experimental tools into trusted components of enterprise financial infrastructure.

The Future of AI Agents in Banking

Banks are at the threshold of AI agent adoption, poised for a transformation well beyond simple automation. As architectures solidify and governance strengthens, banks will leap from fragmented AI tools to powerful, connected agentic ecosystems, ready to drive decisions, coordinate workflows, detect risks, and engage customers instantly.

From isolated bots to multi-agent workforces

Banking’s AI future won’t rely on a single assistant. Instead, banks will unleash expert AI agents that join forces as virtual teams. One agent detects transaction anomalies, while another generates compliance documents. Others empowers relationship managers, and yet another manages all customer communications.

These agents will exchange context, delegate tasks, and escalate issues to humans when needed. Banks will execute complex workflows faster, break down operational silos, and scale high-volume processes while maintaining control.

Read our article on multi-agent orchestration to learn more about managing multiple agents within a single system.

Smart security without moving sensitive data

Future AI agents will also help prevent fraud and cyber threats by enabling safe teamwork. Instead of sending private customer data between banks or markets, organizations will share fraud trends, warning signs, and threat examples in a controlled, anonymous way.

This approach will help banks respond more quickly to new threats while ensuring compliance with data privacy, banking secrecy, and cross-border regulations. In practice, agents will learn from fraud patterns found elsewhere without revealing client information.

Hyper-personalized invisible banking

AI agents will push banking to be proactive and invisible. By interpreting customer behavior, market shifts, and life events in real time, agents pinpoint exact moments to deliver guidance, solutions, or offers.

Customers no longer need to initiate action. Banking agents will detect needs and recommend precise solutions instantly, creating seamless, context-rich, personalized banking woven into every financial moment.

The rise of agent-to-agent commerce

With customers and businesses using their own AI agents, banks must adapt: agent-to-agent finance is the new frontier. A customer’s AI could negotiate mortgages or payments, request funding, or execute transactions with a bank’s AI — directly and autonomously.

This shift will transform digital channels. Banks must now design secure, explainable, and compliant interfaces for seamless agent-to-agent dealings. Trust, authentication, consent, and transparency will underpin this new agent-driven economy.

What does this mean for banks? The future of AI agents in banking is rooted in intelligence, governance, and trust. Banks that invest in robust, secure frameworks today will be primed to automate at scale, hyper-personalize services, and thrive in an AI-driven financial world.

Winners will pinpoint where autonomy adds value, ensure vigilant human oversight, and make every AI-led transaction transparent and compliant.

Conclusion

AI agents are rapidly becoming one of the most important technologies shaping the future of banking. Unlike traditional automation tools, they can reason across complex workflows, coordinate actions across systems, support decision-making, and help financial institutions operate faster, more precisely, and at greater scale.

However, successful adoption is not simply a matter of deploying advanced models. Banks must balance innovation with governance, resilience, security, explainability, and regulatory compliance. The institutions that succeed will be those that build agentic capabilities on a foundation of strong architecture, controlled autonomy, and human accountability.

Whether the goal is accelerating loan underwriting, improving fraud response, reducing compliance workloads, enhancing customer service, or preparing for the next generation of autonomous finance, AI agents offer a practical path toward measurable business outcomes.

Ready to explore how AI agents can transform your banking operations? Contact Emerline's AI experts to discuss your use case and receive a tailored implementation estimate.

Published on Jun 18, 2026