The 2026 U.S. Business Guide to Fintech MVP Development

Table of contents

- Key Takeaways for Tech Leadership

- The Three Non-Negotiable Pillars of 2026 Development

- Market Overview: The 2026 U.S. Landscape

- Critical 2026 Benchmarks

- High-Growth Sectors for 2026 Launches

Key Trends Shaping the U.S. MVP Market- Core Pillars: 2026 Technical Baseline

- 1. Agentic Readiness & KYA

- 2. Atomic Settlements (Instant Clearing)

- 3. Compliance-as-Code & ZKP

- Fintech MVP Development

- MVP Development Costs by Fintech Vertical

- Vertical Deep-Dive: Underlying Cost Drivers

- Neobanking & Digital Wallets

- Lending & Credit-as-a-Service (LaaS)

- WealthTech & Robo-Advisory

- InsurTech Solutions

- The "Hidden" 2026 Compliance Tax (U.S. Specific)

Key Cost Drivers: Impacting Your 2026 Budget- A. Payment Rail Depth & Real-Time Orchestration (+$40k – $60k)

- B. ZKP Implementation & Data Privacy (+$25k – $35k)

- C. AI Explainability & Fairness (+$30k – $50k)

- D. Operational Resilience (DORA-lite Standards) (+15-20% DevOps Effort)

- E. Sponsor Bank Technical Due Diligence (+$15k – $25k)

- Engagement Models: Fintech MVP Development Strategies

- 1. Dedicated Fintech Team

- 2. Staff Augmentation

- 3. Managed MVP / Fixed Price

- 4. Build-Operate-Transfer (BOT)

- Comparison of Approaches (Strategic Matrix 2026)

- Development Roadmap: Concept to Launch (16-18 Weeks)

- Strategic Hubs & Accelerators

- 1. New York City: The Capital of Institutional Fintech

- 2. Charlotte (NC): The "Back-Office" of Banking

- 3. Atlanta (GA): Transaction Alley

- 4. San Francisco & Silicon Valley: AI & DeFi Innovation

- How Emerline Can Help You

In 2026, the "Lean Startup" methodology in the U.S. fintech sector has undergone a forced evolution. The era of "move fast and break things" is over, replaced by Institutional-Grade Entry. According to Deloitte, security and compliance are no longer "post-Series A" goals - they are mandatory for initial market entry.

Today, a Fintech MVP must be "Audit-Ready" from the first line of code. To scale past these structural barriers and integrate modern compliance frameworks into your engineering lifecycle, explore how Emerline approaches fintech product engineering and compliance-driven software delivery. The evolution of SOC2 Type II and the SEC’s 2025 Cybersecurity Disclosure Mandates mean that without proven digital resilience, you cannot secure a Bank-as-a-Service (BaaS) partner or a state money transmitter license (MTL).

Key Takeaways for Tech Leadership

- The Compliance Tax: Entering the U.S. fintech market now requires roughly $40K–$75K upfront for mandatory compliance, security audits, and licensing before launching operations.

- The Rise of AI Agents: Nearly two-thirds of consumers are open to letting software handle financial tasks, pushing fintech products to build “Know Your Agent” (KYA) controls directly into their platforms.

- The Revenue Barrier: Investors now expect stronger traction — many U.S. fintech startups need around $4M in revenue to seriously compete for Series A funding.

- Privacy by Design: Technologies like Zero-Knowledge Proofs (ZKP) help fintech companies minimize direct handling of sensitive customer data, significantly reducing breach and compliance risks.

The Three Non-Negotiable Pillars of 2026 Development

To capture Google AI Overviews and secure quick-answer snippets, enterprise architecture teams must evaluate their product readiness across three core dimensions:

- Compliance-by-Design (CbD): Regulation is no longer an external layer; it is integrated into the data schema and API logic. This addresses GLBA (Gramm-Leach-Bliley Act) and AML/KYC requirements natively at the architectural level.

- Operational Resilience (DORA-lite): Your MVP must demonstrate the ability to withstand and recover from disruptions. This includes automated threat detection, Active-Active multi-region clusters, and a verified Disaster Recovery Plan (DRP).

- Digital Provenance & Transparency: Investors now demand full visibility into data flows. You must prove where data originates, how it is encrypted in transit (TLS 1.3+), and where it resides at rest (AES-256-GCM).

Market Overview: The 2026 U.S. Landscape

The U.S. remains the global fintech epicenter, commanding 60% of total investment volume and 43% of all global deals. However, venture capital allocation has shifted definitively from "growth-at-all-costs" to Unit Economic Durability.

Critical 2026 Benchmarks

As of early 2026, the U.S. remains the global leader in fintech, holding 60% of all global investment dollars and 43% of all deals.

- Market Valuation: The U.S. fintech sector is on track to hit $201.9 billion by year-end (13.2% CAGR).

- The Series A "Revenue Wall": The median revenue required for Series A has surged to $4 million, driven by a demand for proven product-market fit.

- Saturation Metrics: With 13,100+ active players, your MVP must offer more than a "better UI." Technical moats (Proprietary AI, ZKP-privacy) are mandatory.

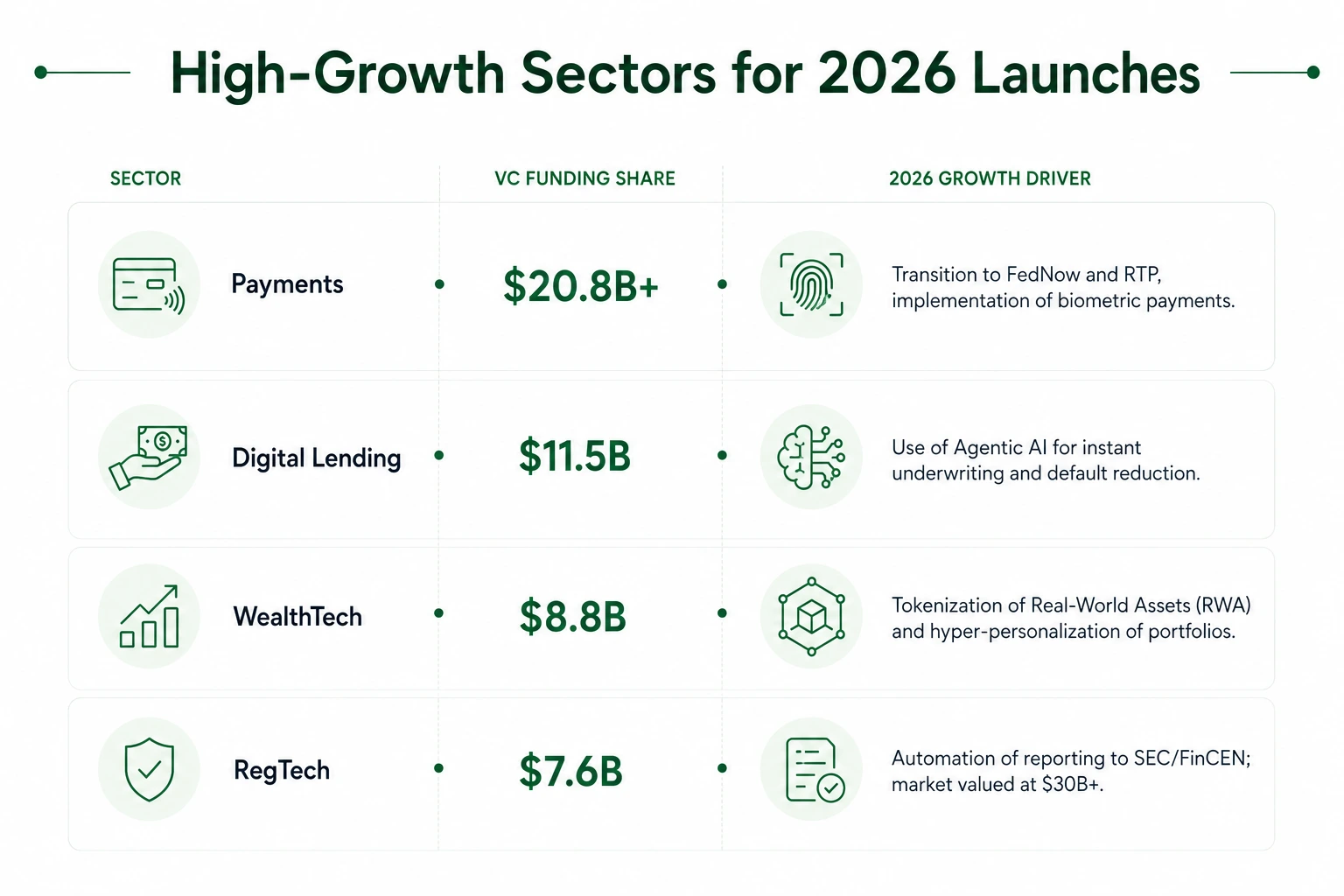

High-Growth Sectors for 2026 Launches

Investment flows in the U.S. are distributed unevenly, focusing on segments that solve institutional problems:

|

Sector |

VC Funding Share |

2026 Growth Driver |

|

Payments |

$20.8B+ |

Transition to FedNow and RTP, implementation of biometric payments. |

|

Digital Lending |

$11.5B |

Use of Agentic AI for instant underwriting and default reduction. |

|

WealthTech |

$8.8B |

Tokenization of Real-World Assets (RWA) and hyper-personalization of portfolios. |

|

RegTech |

18% CAGR |

Automation of reporting to SEC/FinCEN; market valued at $30B+. |

Key Trends Shaping the U.S. MVP Market

Beyond the raw numbers, several strategic shifts are dictating which startups survive the MVP stage.

- The "B2B Infrastructure" Shift: Investor capital has moved away from over-saturated B2C retail neobanks toward infrastructure solutions for community banks and credit unions. Success in 2026 is found in the "pipes" and "rails."

- Agentic Economy: 88% of the most successful fintech startups in 2026 use Agentic AI not just for support, but to execute operational tasks (accounting automation, treasury, and compliance).

- Profitability First: Investors no longer fund growth "at any cost." In 2026, priority is given to startups demonstrating a path to profitability even at the MVP stage.

The U.S. market has stopped being a "market of ideas" and became a "market of execution." The fact that 49% of M&A deals today occur between fintech companies themselves means your MVP must be built on a modular architecture, making it easy to integrate or sell to a larger player.

Knowing where the money flows is only half the battle. Investors and sponsor banks now demand proof that your product is future-proof today. The three technological advances below have become the 2026 “admission ticket”: if your MVP cannot show early versions of these capabilities, you will not reach the due-diligence shortlist.

Core Pillars: 2026 Technical Baseline

Investors and sponsor banks now demand proof that your product is future-proof. Three specific technological advancements have become the "admission ticket":

1. Agentic Readiness & KYA

By 2026, up to 66% of consumers are ready to delegate financial tasks to autonomous agents. Your MVP must support the "Agentic Economy" - an environment where transactions are initiated by software, not humans.

- Know Your Agent (KYA): Similar to KYC, banks now require verification of the AI agents themselves. The protocol must confirm that the agent acts on behalf of a specific individual and has the authority to do so.

- Programmable Authorization: Transitioning from binary access (yes/no) to granular control. The agent receives "Scoped Consent," such as: "Purchase groceries within a $200 weekly limit only at stores with a 4.5+ rating."

- Secure Delegation Protocols: Using standards like AP2 or EMV Click-to-Pay, which allow delegated payments without passing card data directly to the agent.

2. Atomic Settlements (Instant Clearing)

The T+2 settlement system (2-day delay) has officially become a sign of technological backwardness in the U.S.

- FedNow & RTP Mastery: By 2026, the RTP network covers 70% of U.S. accounts, and FedNow has become the standard for small and medium-sized banks. MVPs are required to support both protocols for instant fund disbursement (P2P, payroll, insurance claims).

- ISO 20022 Standard: Adopting this international messaging standard allows rich data to be sent with payments, accelerating compliance checks by 40% and reducing fraud risk.

- Atomic Transactions: Utilizing smart contracts ensures that the exchange of assets and money happens simultaneously - either both actions are completed, or neither is. This eliminates the need for expensive escrow services.

3. Compliance-as-Code & ZKP

With strict privacy laws (CCPA/CPRA in California) and FinCEN anti-money laundering requirements, storing Personal Identifiable Information (PII) has become a massive liability.

- Zero-Knowledge Proofs (ZKP): A technology that allows a user to prove to a bank they are "over 18" or "have an income over $100k" without showing a passport or tax return.

- Liability Reduction: By using ZKP, the fintech company does not store copies of documents. This reduces legal liability by 80% in the event of a data breach, as hackers simply have no access to PII - only to cryptographic confirmations.

- Adaptive Machine-Readable Policies: All compliance is described in code (Compliance-as-Code). If FinCEN updates a sanctions list or limits, the rules in your MVP update automatically via API, eliminating manual labor and errors.

With the technical playbook spelled out, we can now translate features into real-world budgets. The estimates below already bake in the agent-ready, ZKP-enabled, audit-proof architecture described above - so you can plan against 2026 expectations instead of 2021 wishful thinking.

Fintech MVP Development

MVP Development Costs by Fintech Vertical

In 2026, building a Fintech MVP in the U.S. requires more than just code; it requires a "License-Ready" infrastructure. The cost ranges below reflect a senior-level U.S.-based or hybrid squad capable of passing SOC2 audits and integrating with institutional-grade BaaS providers.

|

Vertical |

Functional Focus |

Estimated MVP Budget |

|

Neobanking |

FedNow, Ledger, Biometrics |

$150k – $250k |

|

Lending/LaaS |

AI Explainability, BSA Compliance |

$180k – $300k |

|

WealthTech |

Brokerage APIs, HSM Security |

$200k – $350k |

|

InsurTech |

Claims Automation, Fraud Engine |

$160k – $280k |

Vertical Deep-Dive: Underlying Cost Drivers

Neobanking & Digital Wallets

Estimated MVP Budget: $150,000 – $250,000

2026 Core Requirements: Real-time ledger, FedNow/RTP instant rails, and biometric-secured P2P.

Cost Drivers:

- BaaS Integration ($30k - $50k): Seamless connection with sponsor banks (e.g., Cross River, Coastal) via Unit or Treasury Prime.

- KYC/BSA Automation ($15k - $25k): High-speed identity verification that satisfies the "Travel Rule" for cross-border or digital asset transfers.

Lending & Credit-as-a-Service (LaaS)

Estimated MVP Budget: $180,000 – $300,000

2026 Core Requirements: AI-driven credit scoring, native BSA (Bank Secrecy Act) compliance, and automated loan disbursement rails.

Cost Drivers:

- AI Explainability Layer ($40k+): Building models that comply with 2026 federal transparency laws (requiring "Reason Codes" for any credit denial).

- Credit Bureau Connectivity ($15k): Integrating with Experian, Equifax, or alternative data sources for thin-file scoring.

WealthTech & Robo-Advisory

Estimated MVP Budget: $200,000 – $350,000

2026 Core Requirements: Brokerage API integration, Tax-Loss Harvesting algorithms, and full SOC2 Type II readiness.

Cost Drivers:

- Custody & Settlement Architecture ($50k+): Ensuring digital assets or traditional stocks are held in hardware-secured (HSM) environments.

- Real-time Portfolio Intelligence ($30k): ML engines for personalized asset allocation based on macro-market shifts.

InsurTech Solutions

Estimated MVP Budget: $160,000 – $280,000

2026 Core Requirements: AI-powered claims automation, policy management systems, and IoT data ingestion.

Cost Drivers:

- Claims Fraud Engine ($35k): Using graph analysis to detect fraudulent patterns at the moment of filing.

- Policy Logic Automation ($20k): Complex state-by-state regulation logic embedded into the smart-contract layer.

The headline numbers never show the full invoice. In U.S. fintech there is a parallel cost layer (call it a “compliance tax”) that hits your budget before a single customer can on-board. Mapping these unavoidable items early prevents the 30-40 % overrun that typically appears when the bank’s risk committee asks for “just one more report.”

The "Hidden" 2026 Compliance Tax (U.S. Specific)

When budgeting for a U.S. Fintech MVP, you must account for non-negotiable compliance and security expenses that institutional partners (banks, VCs) will demand before your first transaction.

|

Mandatory Component |

2026 Market Rate (U.S.) |

Impact on Launch |

|

SOC2 Type I Readiness |

$15,000 – $25,000 |

Required for all B2B and BaaS partnerships. |

|

PCI-DSS Level 4 |

$5,000 – $10,000 |

Mandatory for any card data processing. |

|

SEC/FinCEN Registration |

$10,000 – $30,000 |

Legal filing fees and regulatory consulting. |

|

Annual Penetration Test |

$12,000 – $20,000 |

Required by nearly all U.S. sponsor banks. |

Key Cost Drivers: Impacting Your 2026 Budget

The cost of a Fintech MVP is no longer just about the user interface; it is driven by the complexity of the underlying infrastructure and the "Compliance Tax" required by U.S. regulators.

A. Payment Rail Depth & Real-Time Orchestration (+$40k – $60k)

In 2026, integrating with FedNow or The Clearing House (RTP) is more complex than traditional ACH.

- Instant Error Handling: Unlike batch processing, real-time rails require a sophisticated state machine to handle "instant" failures, timeouts, and liquidity exceptions 24/7/365.

- Liquidity Management: Costs are driven by the need for automated treasury modules that ensure the platform has sufficient pre-funded liquidity in the settlement accounts at all times.

- ISO 20022 Compliance: Mapping data to this rich messaging standard is labor-intensive but mandatory for modern rail interoperability.

B. ZKP Implementation & Data Privacy (+$25k – $35k)

Implementing Zero-Knowledge Proofs (ZKP) allows you to verify a user's identity or financial status without ever touching their actual sensitive data.

- Upfront Engineering: This requires specialized cryptography engineering to build "Proof Generation" circuits for your KYC/AML flows.

- Long-term Savings: By not storing PII (Personally Identifiable Information), you significantly lower your insurance premiums and virtually eliminate the $150+ per-record cost associated with potential data breaches under CCPA/CPRA.

C. AI Explainability & Fairness (+$30k – $50k)

Under the U.S. AI Fairness Act of 2025, black-box algorithms for credit scoring are prohibited.

- Transparency Layer: You must build an "Explainability Engine" that provides Reason Codes - legally defensible explanations for why a specific AI-driven financial decision was made.

- Bias Auditing: Budget must be allocated for "Adversarial Testing" to prove your models do not discriminate based on protected classes, a requirement often audited by the CFPB.

D. Operational Resilience (DORA-lite Standards) (+15-20% DevOps Effort)

The OCC and SEC now look for "DORA-style" resilience even in smaller fintechs.

- Multi-Region Active-Active Clusters: To avoid the "single point of failure" risk associated with a single AWS or Azure region, your MVP must run across multiple geographic zones.

- Automated Disaster Recovery (DRP): Costs include the development of "Chaos Engineering" scripts that automatically test and prove your system can recover from a major cloud outage in under 15 minutes.

E. Sponsor Bank Technical Due Diligence (+$15k – $25k)

Bank-Fintech partnerships in 2026 involve deep technical scrutiny.

- Shadow Ledgering: Banks often require you to build a secondary ledger that mirrors their records in real-time to ensure absolute data integrity.

- Audit Documentation: Significant effort is spent preparing "Technical Evidence Packages" for the bank's internal risk committees before you are granted access to their routing transit number (RTN).

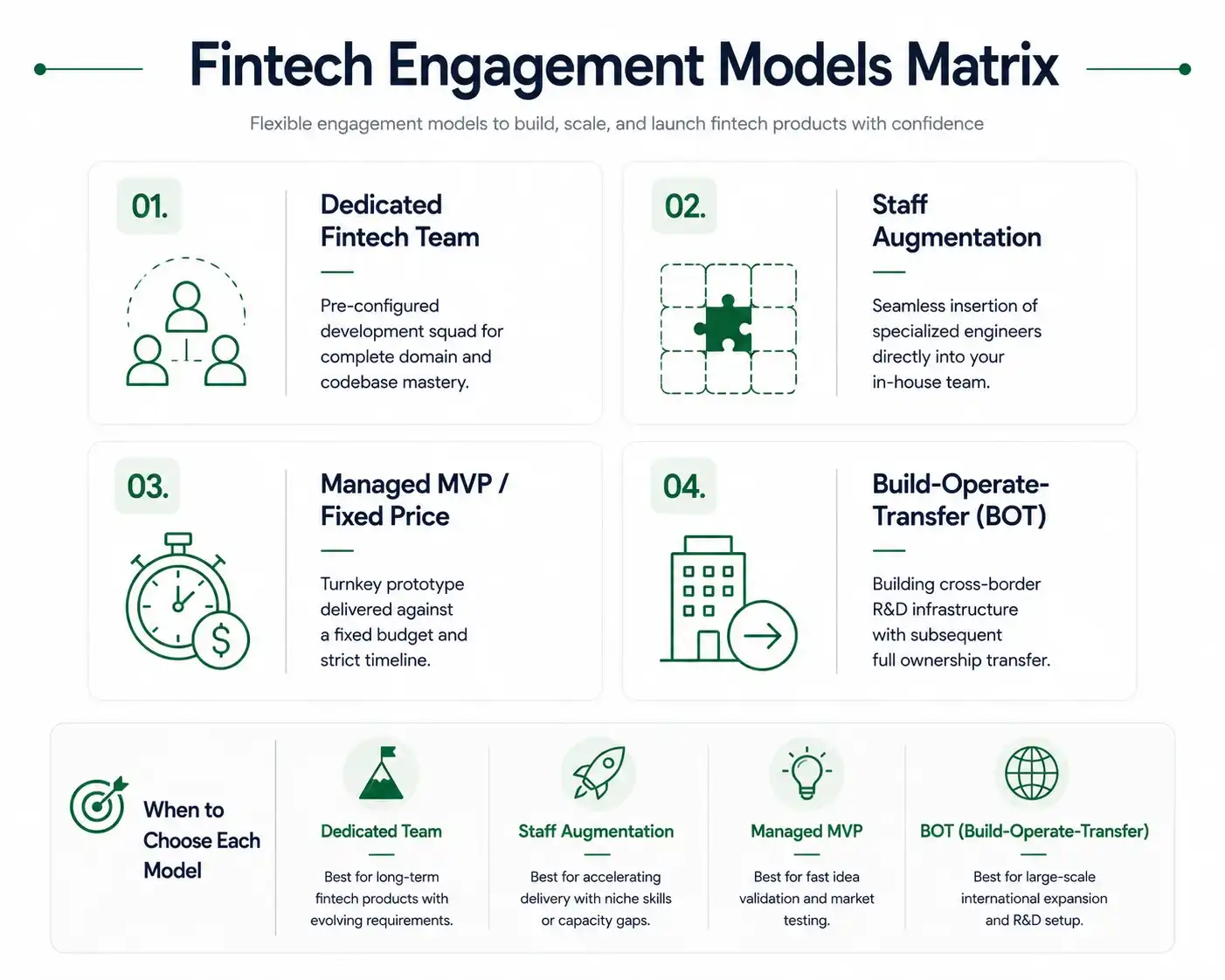

Engagement Models: Fintech MVP Development Strategies

Choosing the correct execution model determines your development velocity and resource allocation flexibility. Learn more about how Emerline structures distributed product teams and delivery workflows in our mobile app development services overview.

1. Dedicated Fintech Team

This is the most popular model for fintech startup app development in 2026. You "rent" a fully staffed team that works exclusively on your project.

- When to choose: If you have a product vision but lack the time or resources to form an in-house team.

- Pros: The team is deeply immersed in the domain (KYC, Ledger, Compliance), knowledge is retained, and processes (Scrum/Agile) are already tuned.

- Risk: Requires constant involvement from the founder or CTO to control business logic.

2. Staff Augmentation

An "enhancement" model where you add individual specialists (e.g., a Rust architect or a security expert) to your existing team.

- When to choose: If you already have a foundation (e.g., a strong backend) but lack specific competencies for launch (e.g., FedNow integration).

- Pros: Maximum control over the process. You manage people directly, just like in-house employees.

- Risk: Responsibility for the final product and the integration of hired employees lies entirely on you.

3. Managed MVP / Fixed Price

"Turnkey" MVP development with a fixed budget and timeline based on a detailed technical specification.

- When to choose: For clearly defined subsystems or prototypes with a limited budget.

- Pros: Financial predictability. All risks of budget overruns lie with the contractor.

- Risk: Minimal flexibility. In 2026, the fintech market changes rapidly; any regulatory change will require contract renegotiation and extra fees.

4. Build-Operate-Transfer (BOT)

A model for long-term scaling: a partner builds the team and product, manages them, and then transfers everything (including legal entities and employees) to your full ownership.

- When to choose: If you plan to create your own R&D center in another jurisdiction but don't want to handle operational routine at the start.

Comparison of Approaches (Strategic Matrix 2026)

|

Criterion |

Dedicated Team |

Staff Augmentation |

Fixed Price |

|

Control Level |

High (via PM) |

Maximum (Direct) |

Medium (Milestones) |

|

Flexibility (Pivoting) |

High |

High |

Low |

|

Speed to Launch |

2-4 weeks |

1-2 weeks |

4-6 weeks (Specs needed) |

|

Target Audience |

Seed/Series A Startups |

Mature Teams |

Micro-Prototypes |

The most effective strategy in 2026 is a Hybrid Start. We recommend starting with a Dedicated Team model for rapid assembly of the MVP core. Once the product is launched and requires focused scaling, you can switch to Staff Augmentation to strengthen specific areas (e.g., Data Science or Cybersecurity) while maintaining full control over the strategy.

Development Roadmap: Concept to Launch (16-18 Weeks)

Our optimized process accelerates Time-to-Market for the U.S. ecosystem:

- Discovery & Regulatory Mapping (2-3 Weeks): Market research, choosing between a de novo license or a BaaS partner (e.g., Coastal, Cross River).

- Architecture Design (3-4 Weeks): Selecting cloud infrastructure (AWS FinServ/Azure for FSI) and designing the immutable ledger.

- Development Sprints (8-10 Weeks): Iterative feature builds and integration with U.S. rails (Plaid, Stripe, FedNow).

- Security Audit & Hardening (2-3 Weeks): Red Team attacks, SOC2 readiness, and final bug resolution.

- Deployment & Launch: Scalable release within a high-compliance production environment.

By week 18 you will have a launch-ready product, but you will also need an ecosystem - accelerators, regulators, potential acquirers and next-round investors. The four hubs below each specialize in a different slice of fintech infrastructure; choosing the right city can shorten partnership cycles by months and put you inside the regulatory feedback loop before your competitors even file their first form.

Strategic Hubs & Accelerators

Launch success often depends on your ecosystem. In 2026, the U.S. market is segmented by specialization: New York for Institutional B2B, Charlotte for Banking Back-Office, Atlanta for Transaction Rails, and Silicon Valley for AI Innovation.

1. New York City: The Capital of Institutional Fintech

NYC in 2026 is "ground zero" for startups working with banking giants and requiring complex compliance.

- Key Accelerator: FinTech Innovation Lab. Direct access to C-level executives from 40+ major banks (J.P. Morgan, Goldman Sachs).

- Strategic Advantage: Ideal for RegTech, Agentic AI, and enterprise B2B solutions.

2. Charlotte (NC): The "Back-Office" of Banking

The second-largest banking center in the U.S. (headquarters of Bank of America).

- Key Accelerator: Fintech Generations.

- Strategic Advantage: Local investors understand long sales cycles (9–18 months) and are a perfect fit for Banking Infrastructure startups.

3. Atlanta (GA): Transaction Alley

Atlanta processes over 70% of all card transactions in the U.S.

- Key Accelerator: FinTech Atlanta. A coalition helping to integrate with giants like NCR and Fiserv.

- Strategic Advantage: The best environment for implementing instant payments via FedNow and RTP.

4. San Francisco & Silicon Valley: AI & DeFi Innovation

The leader for projects at the intersection of fintech, DeFi, Deep AI, and Web3 infrastructure.

- Key Accelerator: Y Combinator (Fintech Track). Highest checks and a focus on autonomous financial agents.

- Strategic Advantage: Access to cutting-edge AI technologies and capital ready for high risks.

You now have the market numbers, the technical blueprint, the budget, the delivery model, the timeline and the ecosystem map. The final piece is the execution partner who can guarantee that all of those pieces fit together without hidden gaps. Emerline acts as that single point of accountability - delivering not just code, but the documentation, audit artifacts and bank-grade integrations your MVP needs to pass third-party risk committees on the first attempt.

How Emerline Can Help You

Emerline acts as your strategic partner in the U.S. market, delivering not just code, but technological superiority. We bridge the gap between ambitious Fintech visions and high-performance, market-ready realities by providing deep domain expertise at every stage of development.

- Future-Proof Architecture: We design products that meet "2030 standards," ensuring your technical foundation is resilient enough to handle future federal shifts and evolving regulatory demands.

- Institutional-Grade Integration: Our teams build systems natively compatible with FedNow/RTP rails and institutional audit requirements, clearing the path for seamless bank partnerships.

- Full-Cycle Strategic Support: From initial compliance mapping to scaling a secure production environment, we provide the consulting and engineering power necessary to navigate the complexities of the 2026 financial landscape.

Ready to build the future of finance? Contact us to book your MVP Strategy Session.

Disclaimer: This material is for informational purposes only and does not constitute legal or financial advice. U.S. regulatory requirements (SEC, FinCEN) are subject to change. We recommend a professional compliance audit before any public launch.

Updated on Jun 4, 2026