What Is Open Banking? Definition, Use Cases, and Market Outlook

Table of contents

- Open Banking Explained: How the Model Works

- Traditional banking vs open banking

- Open banking vs open finance

- How Open Banking Operates in Practice

- The open banking process: step by step

- What data is typically shared in open banking?

- Is open banking safe?

- How Open Banking Stakeholders Interact

- Typical integration models

- Practical Open Banking Use Cases

- Bank account verification

- Lending and underwriting

- Personal finance and cashflow intelligence

- Payments and recurring payments

- Open Banking Worldwide: From Regulation to Scale

- The open banking market: size, trajectory, and momentum

- Regional dynamics: how open banking evolves across markets (2026–2030)

- Risk assessment: structural challenges through 2030

- Strategic recommendations for building in an open finance world

- Trends and Predictions: Open Banking From 2026 to 2030

- Open banking expands into open finance

- Regulation remains the biggest swing factor in the US

- AI becomes the true differentiator

- Standardization accelerates the reduction of fragmentation

- The rise of account-to-account payments

- Trusted identity verification via banking rails

- Conclusion

Open banking is a regulated system for sharing financial data through secure APIs, allowing customers to decide how their banking information is used. With explicit user consent, banks securely share account and transaction data with licensed third parties, enabling more transparent, competitive, and personalized financial services.

For financial institutions, open banking enables rapid product innovation and broader partnerships; for end users, it offers smarter money management, easier access to credit, and streamlined digital experiences. This transition is tangible: the global market is accelerating, with projections indicating a $135.2 billion valuation by 2030, fueled by regulation, mature APIs, and rising consumer demands.

Open banking frameworks are designed with strong data protection controls. Information is shared solely with the customer’s explicit approval and is protected by strict regulations and robust technical safeguards to prevent misuse or unauthorized access.

Key takeaways:

- Open banking is evolving into open finance, expanding data-sharing beyond payments into investments, insurance, and identity.

- Global adoption is accelerating, with Europe, North America, and Asia-Pacific following distinct but converging paths.

- Regulation remains a critical driver and risk factor, requiring architectures that can adapt to change.

- AI is becoming the primary differentiator, transforming raw financial data into real-time decisions and automation.

- Account-to-account payments and bank-based identity verification are moving into the mainstream.

- Long-term success depends on orchestration (coordinating diverse data, systems, and processes), security, and data intelligence, not just on aggregation (simply collecting data).

Open Banking Explained: How the Model Works

To provide a precise open banking definition, it is a framework in which financial institutions make selected customer data, such as account balances, transactions, or payment initiation capabilities, available to authorized third parties via standardized application programming interfaces (APIs). This access is granted only when a customer explicitly consents and can be revoked at any time.

In practice, banks act as secure data stewards, while fintechs, merchants, and financial service providers develop value-added solutions using that data. These solutions include budgeting tools, alternative credit scoring, instant payments, and unified financial dashboards. APIs replace unreliable screen scraping, ensuring consistent data, predictable performance, and enhanced security.

A simple open banking example illustrates this in action: a personal finance app aggregates accounts from multiple banks into a single interface. Instead of manually uploading statements, users authorize the app to retrieve data directly from their banks, creating a real-time, accurate view of their finances.

Technically, open banking relies on strong customer authentication, token-based access, audit logging, and regulatory monitoring. For businesses, it enables new revenue streams, streamlines customer onboarding, and accelerates product delivery to market.

Traditional banking vs open banking

Traditional banking operates on closed systems. Customer data is usually siloed within a single institution, and integration with external providers is rare, customized, or nonexistent. Innovation moves slowly, and customers often need to change banks to access better features or products.

Open banking reverses this pattern. Data portability becomes a customer right, not an exception. Customers can blend services from multiple providers without leaving their main bank, while institutions compete on experience, pricing, and insights rather than just data ownership. This transformation lowers barriers for new entrants and pushes incumbents to modernize.

Where traditional banking protects institutional control, open banking solutions empower customers without sacrificing regulatory compliance or security standards.

Open banking vs open finance

Open banking focuses specifically on payment accounts and core banking data, such as balances, transactions, and payment initiation.

Open finance extends this concept further. It encompasses a broader spectrum of financial products, including investments, pensions, insurance, mortgages, and even non-bank financial data. In this sense, open banking is the foundation of open finance.

Understanding this distinction is essential when analyzing open banking growth or evaluating the long-term market size. Open banking forms the first and most advanced layer of a larger transformation in financial data movement.

How Open Banking Operates in Practice

Open banking is often discussed as a regulatory framework or a digital capability, but its real value lies in how data exchange actually occurs: from a user’s decision to connect an account to the final financial outcome delivered by an application. Behind the scenes, this flow is carefully orchestrated to balance convenience, control, and compliance.

The open banking process: step by step

Step 1: The user chooses a service

The journey begins when a customer selects a product that uses open banking, such as a budgeting app, credit platform, or verification tool. The app explains why data access is needed and what benefits, such as faster onboarding, tailored insights, or seamless payments, the user will receive.

This initial moment is critical because it establishes transparency and trust. If the value proposition is unclear, customers are unlikely to proceed.

Step 2: Consent is granted

Once the user agrees to proceed, they are redirected to their bank’s authentication environment. There, they log in with existing credentials and approve permissions, such as sharing transaction history or confirming account ownership.

Consent is granular, so users approve only what is needed. This minimizes data sharing and gives customers clear control.

Step 3: Data is shared via APIs

After consent, the bank transmits the requested data through secure APIs. These replace outdated, unsafe methods like credential sharing or screen scraping.

Each request is authorized with time-limited tokens and logged for accountability across participants.

Step 4: Data is normalized and processed

Raw banking data is rarely usable as is. Institutions format information differently, making normalization essential. Here, the data is cleaned, structured, and enriched for consistent interpretation.

This processing layer powers intelligence such as categorizing transactions, detecting income patterns, and identifying behavioral signals otherwise hidden in statement line items.

Step 5: Outcome is delivered

The application then translates processed data into results such as instant identity verification, a credit decision, a personalized recommendation, or a completed payment.

From the user’s perspective, this entire chain of events often takes only a few seconds, yet behind it sits a carefully governed ecosystem designed to balance speed, accuracy, and compliance.

What data is typically shared in open banking?

Open banking data access goes beyond surface-level account details. It provides a nuanced financial picture that supports decision-making across lending, payments, and personal finance.

Account data includes account identifiers, type, currency, and ownership information. This is often used for onboarding, account verification, and linking financial products.

Balance data provides real-time or near-real-time visibility into available funds. It plays a critical role in affordability checks, risk monitoring, and payment authorization.

Transaction data provides a historical record of incoming and outgoing payments. This is one of the most valuable datasets, as it reveals income patterns, spending behavior, and financial stability over time.

Behavioral signals are derived rather than directly shared. These can include indicators such as income consistency, recurring obligations, or early signs of financial stress, helping platforms move beyond static scoring models.

Together, these layers form the backbone of many modern financial products built on open banking.

Is open banking safe?

Although open banking introduces a new way to exchange financial data, it is not an unregulated experiment. In fact, it is one of the most tightly governed digital finance frameworks currently in operation.

Different regions have established formal standards and oversight mechanisms to ensure security and consumer protection. In the United States and Canada, the Financial Data Exchange (FDX) standard defines how data should be shared responsibly. In the UK, the Financial Conduct Authority (FCA) supervises the ecosystem, while in the European Union, PSD2 sets strict requirements for authentication, consent management, and third-party licensing.

Open banking can reduce risks associated with credential sharing compared to legacy methods: customers don’t share their banking credentials with third parties, permissions are limited, and all activity is logged and auditable.

The result is a system designed not only for innovation but also for controlled, accountable data sharing.

How Open Banking Stakeholders Interact

Open banking is not driven by a single entity. It is a coordinated ecosystem where multiple participants collaborate to deliver value while sharing responsibility for security, reliability, and compliance.

Customer (end user)

The customer remains at the center of the ecosystem. They decide whether to connect their accounts, which permissions to grant, and when to revoke access. In open banking, data ownership shifts from the institution to the individual.

Bank/ASPSP (data holder)

The bank is responsible for authenticating the user, enforcing consent boundaries, and exposing data through regulated APIs (Application Programming Interfaces, which are software protocols that allow different systems to communicate securely). It remains the system of record and controls how and when information can be accessed.

Banks safeguard credentials and ensure only licensed providers can access data.

Third-party provider/application

The third-party application is the service the customer actually interacts with. It explains the purpose of data sharing, initiates the consent flow, and transforms banking data into functional features such as lending decisions or financial dashboards.

This layer owns the customer experience, managing functionality, communication, usability, and support.

Open banking platform/aggregator

Some ecosystems include an intermediary platform that connects to multiple banks on behalf of applications. This layer simplifies integration, normalizes data formats, and handles technical variations between institutions.

Aggregators can add monitoring and resilience, reducing development overhead.

Regulators and standards bodies

Regulators establish the legal framework that governs the ecosystem. They define how consent works, how security must be implemented, and what rights consumers have over their data.

While they do not participate directly in each transaction, their influence shapes every technical and operational decision.

Typical integration models

Direct-to-bank integrations are suitable for limited geographies or a small number of institutions. They offer maximum control but require substantial engineering effort and ongoing maintenance.

Aggregator-first integrations provide rapid coverage across many banks. They reduce complexity but introduce dependency and less flexibility over edge cases.

Hybrid architectures combine both approaches, including direct connections for priority banks and aggregators for the long tail. This model often delivers the best balance between performance, cost, and reliability.

Many mature products ultimately evolve toward a hybrid setup, using redundancy to improve uptime and user experience when individual connections degrade.

Practical Open Banking Use Cases

Open banking moves from theory to value only when it solves concrete user problems. In production environments, its success is measured not by API calls but by faster onboarding, better decisions, lower failure rates, and improved customer trust. Below are the most common and commercially proven open banking use cases, broken down by user intent, data inputs, operational mechanics, and real-world performance indicators.

Bank account verification

User goal

Confirm that a bank account is genuine, active, and owned by the person attempting to use it, so payments, payouts, or disbursements can proceed without delays or avoidable failures.

Data used

With explicit customer consent, open banking connections can surface:

- Core account identifiers and status signals (open, closed, restricted)

- Ownership or account-holder confirmation indicators (where supported)

- Presence of a positive account balance and recent transaction activity, used when assurance is needed that the account is actively in use

How open banking enables it

Traditional verification uses manual entry, micro-deposits, or document uploads. Open banking replaces these with direct, source-level confirmation:

- Users authenticate through their bank’s native login experience

- Verified account details are returned directly from the institution

- Ownership signals reduce ambiguity without exposing sensitive credentials

- Verification completes in a single session rather than over days

This significantly lowers onboarding friction while improving data confidence.

Success metric

- High verification completion rate once users initiate the flow

- Median time to verified account measured in minutes, not days

- Measurable reduction in failed first payments or returned payouts

Supporting indicators often include consent completion rates, authentication success by bank, and “verified but unusable” account ratios.

Examples

- Marketplace onboarding to enable seller payouts

- Lending platforms validating disbursement accounts

- Payroll and gig-economy systems setting up worker payments

Common pitfalls

Drop-off occurs if the value is unclear or if bank authentication flows are not designed. Teams should monitor funnel performance by institution and spot-to-spot friction points.

Lending and underwriting

User goal

Receive faster, fairer credit decisions without uploading documents, while lenders assess affordability and risk using real financial behavior rather than static snapshots.

Data used

With applicant consent, open banking can provide:

- Transaction histories highlighting income, expenses, and obligations

- Account balances and volatility indicators

- Signals of existing commitments such as loans, rent, or subscriptions

- Consistency markers, including salary regularity or self-employed seasonality

How open banking enables it

Instead of relying solely on bureau scores or PDFs, lenders can:

- Access real cashflow data in near real time

- Automate affordability checks using standardized rules

- Distinguish sustainable income from one-off deposits

- Reduce manual review by applying consistent logic across applicants

This speeds decisions and smooths the application process.

Success metric

- Reduced time from application to decision

- Higher approval rates at stable risk levels

- Lower manual review rates without increased defaults

Supporting metrics often include data usability rates and consent completion performance.

Examples

- Personal lending and point-of-sale financing

- SME and freelancer credit assessment

- Dynamic credit line management

Common pitfalls

Misclassified transactions distort the results. Strong categorization, explainability, and fall-backs are key when data is incomplete or unclear.

Personal finance and cashflow intelligence

User goal

Understand spending behavior, anticipate cash shortfalls, and make better day-to-day financial decisions without manual tracking.

Data used

- Transactions across one or multiple accounts

- Current and historical balances

- Enriched merchant and category data

- Timing signals such as pay cycles and recurring bills

How open banking enables it

Open banking provides the breadth and continuity of data needed to:

- Aggregate accounts into a unified financial view

- Power budgeting, categorization, and trend analysis

- Enable predictive insights, such as balance forecasting

- Trigger timely alerts for anomalies or upcoming obligations

Success metric

- Short time-to-first-meaningful insight after connection

- Strong engagement and retention among connected users

- High alert interaction rates and reduced negative financial events

Examples

- Consumer budgeting and money-management apps

- Digital banks expanding beyond basic accounts

- SME dashboards tracking short-term liquidity

Common pitfalls

Unreliable data reduces credibility. Monitor data freshness and communication delays clearly to preserve trust.

Payments and recurring payments

User goal

Pay directly from a bank account with fewer intermediaries, and manage recurring payments with greater transparency and reliability.

Data used

- Payment initiation capabilities (where supported)

- Account validation and payer identity signals

- Consent-based recurring payment constructs

- Payment status and confirmation data

How open banking enables it

Compared to card-only models, open banking payments can:

- Offer pay-by-bank options aligned with customer preferences

- Reduce failures caused by expired or reissued cards

- Improve reconciliation through richer payer metadata

- Give customers clearer control over recurring authorizations

Success metric

- Strong conversion rates for pay-by-bank options

- High first-payment success rates

- Lower cost-to-collect where fees are reduced

- Reduced involuntary churn for recurring billing

Operational metrics include authorization completion, bank coverage, and refund turnaround time.

Examples

- E-commerce checkouts adding bank-based payments

- Subscription platforms reducing payment failures

- Marketplaces managing both collections and payouts

Common pitfalls

Bank experiences vary by region. Use clear messaging, trust signals, and fallback payment methods when bank flows are inconsistent or fail.

Open Banking Worldwide: From Regulation to Scale

Open banking has moved well beyond its early regulatory origins and is now shaping a broader global transition toward open finance. Between 2025 and 2030, market growth will no longer be driven solely by compliance but by commercial adoption, real-time payment rails, and data-driven financial services. What emerges is a fragmented yet rapidly converging global map, where regions evolve at different speeds but toward similar outcomes: interoperability, consumer-controlled data, and programmable financial infrastructure.

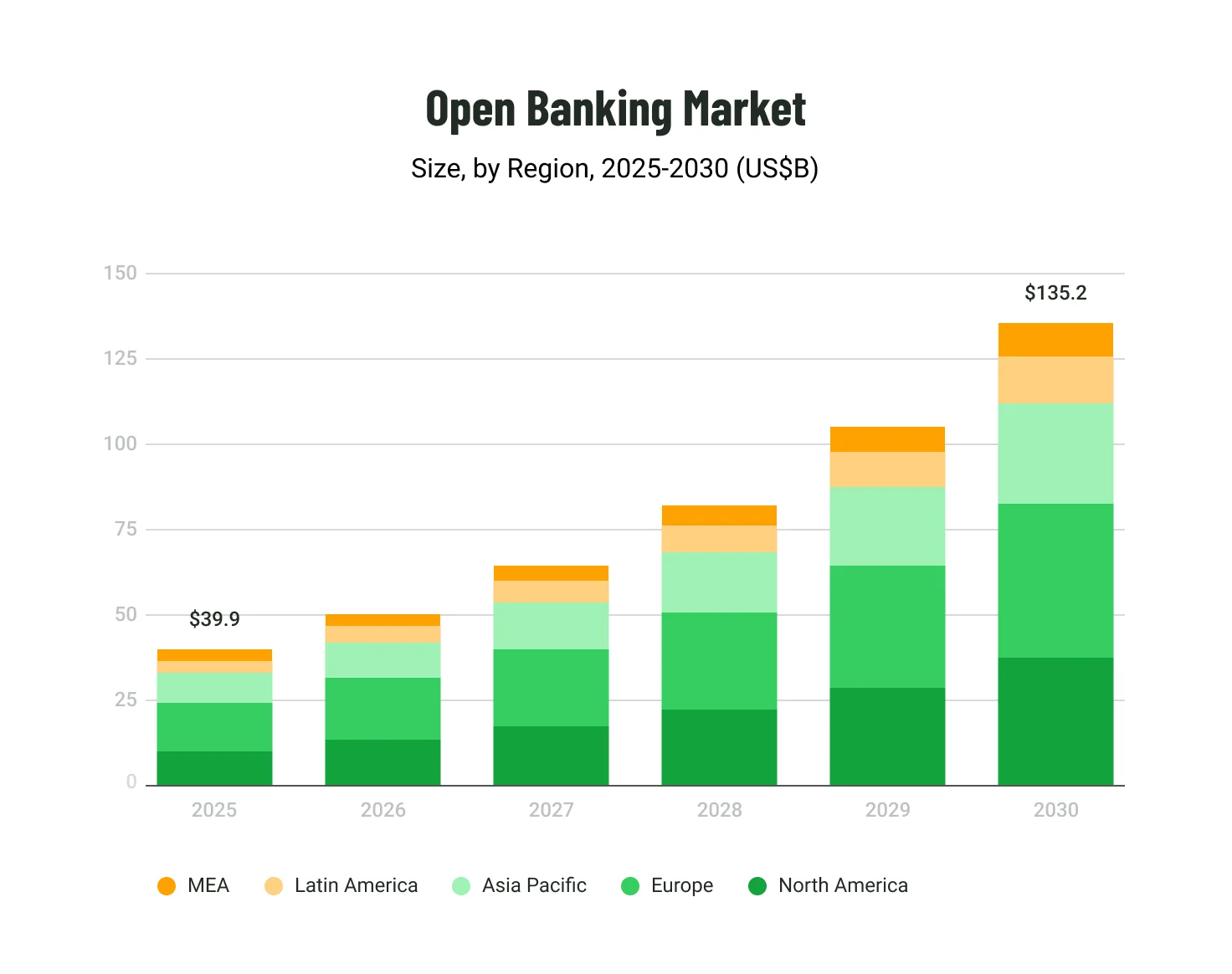

The open banking market: size, trajectory, and momentum

The global open banking market is entering an accelerated phase of expansion. Industry research shows that growth through the second half of the decade is fueled by three converging forces: regulatory mandates, consumer demand for connected financial experiences, and the maturation of API-based banking infrastructure.

While early adoption was concentrated in Europe, the market’s center of gravity is shifting. From 2025 onward, North America and Asia-Pacific account for an increasing share of total volume, driven by large-scale consumer usage, embedded finance, and account-to-account payment adoption.

By 2030, the market is projected to scale to $135.2 billion globally, with a steep growth curve visible even in the 2025–2030 window. The chart accompanying this section illustrates not just expansion, but acceleration, each year adding more value than the last as open banking capabilities move from niche integrations into core financial rails.

Regional dynamics: how open banking evolves across markets (2026–2030)

Although open banking operates on common principles, its practical shape varies significantly across regions. Regulation, infrastructure maturity, and consumer behavior combine to create distinct growth patterns.

Below is a comparative table highlighting regional market size in 2024, projected value by 2030, and the primary growth driver shaping adoption.

| Region | 2024 Market Size | 2030 Projected Value | Primary Growth Driver |

| North America | $8.6B | $37.6B | CFPB Section 1033 & B2B Lending Innovation |

| Europe | $12.4B | $43.2B | PSD3/PSR & The FiDA Framework |

| Asia-Pacific | $7.4B | $29.4B | UPI Evolution & Smart City Interoperability |

| LATAM | $2.1B | $8.5B | Financial Inclusion & Pix-led Ecosystems |

Europe: standardizing the second wave

Europe remains the regulatory reference point for open banking, but the focus is shifting from access to quality. By 2026, the industry is preparing to implement PSD3, which aims to address long-standing issues such as API fragmentation, inconsistent uptime, and uneven performance across banks. The emphasis is no longer on whether data should be shared, but on how reliably and uniformly that sharing works in practice.

Alongside PSD3, the Financial Data Access (FiDA) framework marks a structural expansion of scope. Mortgages, investment accounts, pensions, and insurance data are brought into the same regulatory logic, effectively transforming open banking into a full open finance ecosystem. For product teams, this means a broader surface area for innovation but also higher expectations around consent management, data accuracy, and cross-domain interoperability.

North America: the API standardization era

In the United States, the market is undergoing a foundational shift. Regulatory pressure following CFPB mandates in 2024–2025 (rules from the Consumer Financial Protection Bureau) has accelerated the transition away from credential-based screen scraping (a method where systems collect user data by accessing their online banking using their username and password) toward tokenized, permission-driven API access (a secure process where access is granted through digital tokens and controlled by user permissions, rather than passwords). This change reduces systemic risk while enabling more consistent, auditable data flows.

Consumer adoption is already substantial. Research indicates that roughly 87% of U.S. consumers have used open banking-enabled connections to link accounts with third-party applications, particularly in fintech lending, budgeting tools, and wealth management platforms. The next phase of growth hinges on standardization rather than access, making interoperability and developer experience the competitive battleground.

Asia-Pacific: the real-time leader

Asia-Pacific is the most operationally advanced region in real-time financial infrastructure. Systems such as India’s UPI demonstrate how account-to-account payments can scale nationally, processing tens of billions of dollars annually and supporting everyday consumer use cases.

The region is projected to be the fastest-growing open banking market through 2030, with a CAGR approaching 30%. This momentum is driven by mobile-first populations, government-backed payment rails, and widespread acceptance of bank-based authentication. APAC’s trajectory suggests a future in which open banking is not a feature layer but the default for payments, identity verification, and financial orchestration.

Emerline strategic insight: As markets mature, value shifts upstream. Competitive advantage increasingly lies in data enrichment, using AI to transform raw transaction strings into actionable insights such as subscription detection, affordability signals, or pre-approved offers before data even reaches the user interface.

Risk assessment: structural challenges through 2030

| Challenge | Impact | Strategic Evolution | Mitigation Strategy |

| API Latency | Medium | Transition to gRPC and Event-Driven APIs. | Target <50ms latency for real-time streaming. |

| Deepfake Fraud | Critical | Fraud attempts surged 2,137% since 2023. | Implement Behavioral Biometrics and liveness detection. |

| Consent Fatigue | Medium | Regulatory mandate for Consent Dashboards in PSD3. | Build a "Single Pane of Glass" for all data sharing permissions. |

| Cybersecurity | High | Rising cyberattacks targeting API gateways. | Shift to mTLS (Mutual TLS) and zero-trust orchestration. |

As open banking scales, so do its systemic risks. Between 2026 and 2030, several pressure points consistently emerge across regions.

API latency and reliability remain operational concerns, especially where banks control authentication and uptime. Consent fatigue threatens engagement as users are asked to authorize multiple connections across services. Cybersecurity risks evolve as attackers leverage AI-generated fraud techniques, including deepfake-enabled social engineering.

A structured risk assessment matrix, a tool that lists and evaluates risks by their impact, how they might evolve, and relevant mitigation strategies, helps teams plan defensively rather than reactively.

Emerline strategic insight: Trust is rapidly becoming the primary differentiator. With AI-enabled fraud losses projected to reach $40 billion by 2027, platforms that make security controls visible, understandable, and user-centric will capture disproportionate market share.

Strategic recommendations for building in an open finance world

As open banking transitions into open finance, strategy matters as much as compliance.

Forward-looking teams are moving beyond pure aggregation (collecting financial data) toward orchestration layers – systems that not only retrieve data, but initiate actions such as payments, credit decisions, and identity verification. In Europe, early alignment with PSD3 requirements (the upcoming European payment services regulations), like payee name verification and enhanced IBAN (International Bank Account Number) checks, reduces future remediation costs.

Globally, investment in account-to-account payment rails (platforms that move money directly between bank accounts, such as SEPA Instant in Europe and FedNow in the US) is becoming essential as businesses seek to reduce their dependence on high-fee card networks and enable real-time settlement.

Trends and Predictions: Open Banking From 2026 to 2030

As open banking matures into open finance, the conversation shifts from access to advantage. The years between 2026 and 2030 will be defined not by who can connect to financial data, but by who can interpret it responsibly, act on it intelligently, and adapt to regulatory and technological change without disrupting users or operations. The trends below outline how the open banking landscape is expected to evolve and where forward-thinking organizations should focus their investment.

Open banking expands into open finance

The coming years will see a formal shift from payment-account-centric data sharing toward a broader financial data framework. In the EU, proposed open finance legislation extends consumer data rights across investment, insurance, and pension products, fundamentally changing how financial ecosystems interconnect.

Regulation remains the biggest swing factor in the US

Unlike Europe’s prescriptive approach, U.S. regulation remains fluid. Legal challenges and revisions to Section 1033 (a part of U.S. law governing consumer access to financial data) mean timelines and requirements can change with little notice. Product teams targeting the U.S. market must design for regulatory volatility, not stability.

AI becomes the true differentiator

By 2026, access to open banking data will be table stakes. Differentiation comes from interpretation.

Advanced analytics layers convert transaction data into real-time decisions, personalized risk controls, and proactive financial guidance. Agentic AI is already reshaping personal finance management, moving from static dashboards to systems that act autonomously, transferring surplus funds, optimizing savings, or adjusting credit exposure based on live cash flow.

Banks adopting AI development co-pilots (software tools that assist developers using artificial intelligence) report productivity gains of up to 40%, accelerating feature delivery across open banking products.

Emerline strategic insight: Embedding AI directly into open banking infrastructure enables adaptive credit models that learn continuously from behavioral data, reducing default risk without increasing friction.

Standardization accelerates the reduction of fragmentation

Fragmentation is increasingly seen as a commercial liability. In North America, initiatives such as FDX demonstrate growing alignment around interoperable standards. In Europe, regulatory pressure continues to push banks toward consistent APIs and service levels. Globally, the trend favors fewer standards, clearer rules, and stronger enforcement.

Emerline strategic insight: Architect for change. Modular compliance gateways allow teams to adapt quickly to regulatory shifts, whether under Section 1033 or EU directives, without rebuilding core systems.

The rise of account-to-account payments

A2A payments are transitioning from alternative to default. User adoption is projected to grow from roughly 183 million in 2025 to more than 645 million by 2029. Businesses benefit from dramatically lower transaction costs, often up to 80% lower than card-based payments, while real-time settlement via SEPA Instant and FedNow reshapes cash flow dynamics.

Trusted identity verification via banking rails

Open banking is increasingly used as a primary identity signal. Bank-verified credentials enable seamless age and identity checks without document uploads, reducing KYC costs by up to 50% while improving conversion rates and user trust.

Conclusion

Open banking is no longer standalone; it is the connective tissue of modern financial ecosystems. As open finance emerges, success depends on navigating AI-driven intelligence, resilient security, and evolving regulations across regions.

This is where execution matters as much as vision. Building for the next decade requires more than compliant APIs; it demands infrastructure that can scale across markets, analytical layers that convert raw data into decisions, and security models designed for an era of AI-enabled fraud.

Emerline helps financial organizations navigate this transition with confidence by combining deep fintech engineering with practical regulatory awareness. From designing high-throughput API gateways aligned with PSD3 and CFPB expectations, to applying advanced data enrichment models that power credit scoring and personal finance experiences, to conducting rigorous security and resilience assessments that address modern attack vectors, Emerline focuses on making open finance systems dependable, adaptable, and commercially effective.

Move decisively beyond data access and build competitive, insight-driven financial products. Contact Emerline’s open finance experts now to secure your 2030 market lead.

Published on Feb 18, 2026